Adjusting entries 2

For now we want to highlight some important points.

There are two scenarios where adjusting journal entries are needed before the financial statements are issued:

- Nothing has been entered in the accounting records for certain expenses or revenues, but those expenses and/or revenues did occur and must be included in the current period's income statement and balance sheet.

- Something has already been entered in the accounting records, but the amount needs to be divided up between two or more accounting periods.

Adjusting entries almost always involve a

- balance sheet account (Interest Payable, Prepaid Insurance, Accounts Receivable, etc.) and an

- income statement account (Interest Expense, Insurance Expense, Service Revenues, etc.

Adjusting Entries - Liability Accounts

Notes Payable $5,000Notes Payable is a liability account that reports the amount of principal owed as of the balance sheet date. (Any interest incurred but not yet paid as of the balance sheet date is reported in a separate liability account Interest Payable.) The accountant has verified that the amount of principal actually owed is the same as the amount appearing on the preliminary balance sheet. Therefore, no entry is needed for this account.

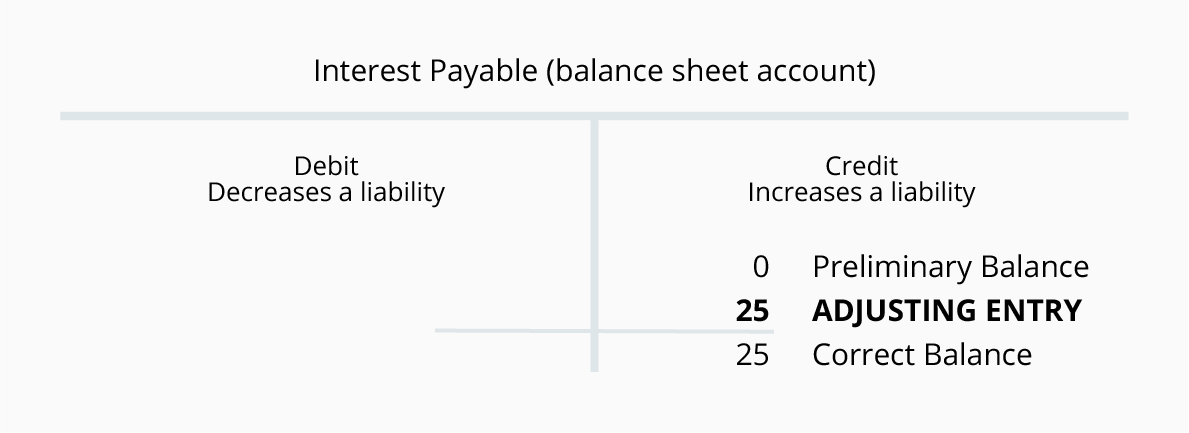

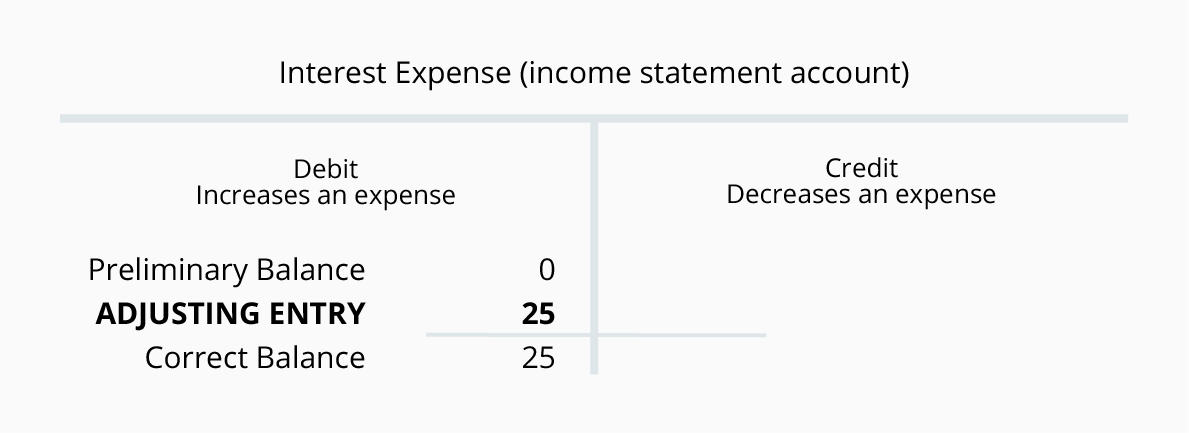

Interest Payable $0

(It's common not to list accounts with $0 balances on balance sheets.)

Interest Payable is a liability account that reports the amount of interest the company owes as of the balance sheet date. Accountants realize that if a company has a balance in Notes Payable, the company should be reporting some amount in Interest Expense and in Interest Payable. The reason is that each day that the company owes money it is incurring interest expense and an obligation to pay the interest. Unless the interest is paid up to date, the company will always owe some interest to the lender.

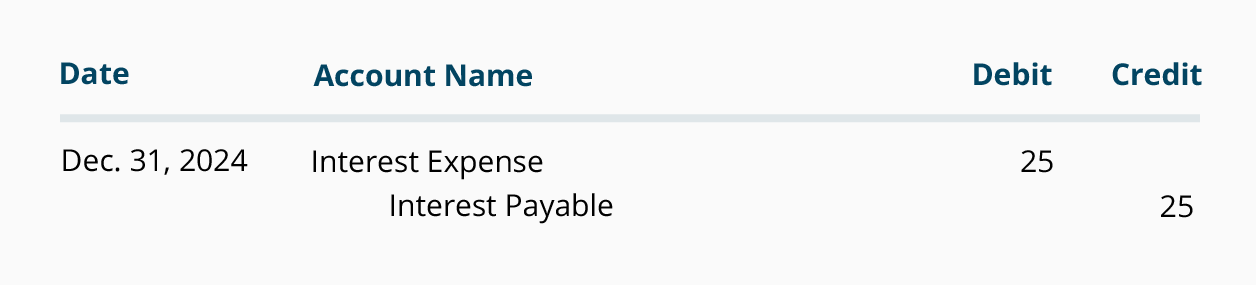

Let's assume that the company borrowed the $5,000 on December 1 and agrees to make the first interest payment on March 1. If the loan specifies an annual interest rate of 6%, the loan will cost the company interest of $300 per year or $25 per month. On March 1 the company will be required to pay $75 of interest. On the December income statement the company must report one month of interest expense of $25. On the December 31 balance sheet the company must report that it owes $25 as of December 31 for interest.

The adjusting journal entry for Interest Payable is:

It is unusual that the amount shown for each of these accounts is the same. In the future months the amounts will be different. Interest Expense will be closed automatically at the end of each accounting year and will start the next accounting year with a $0 balance.

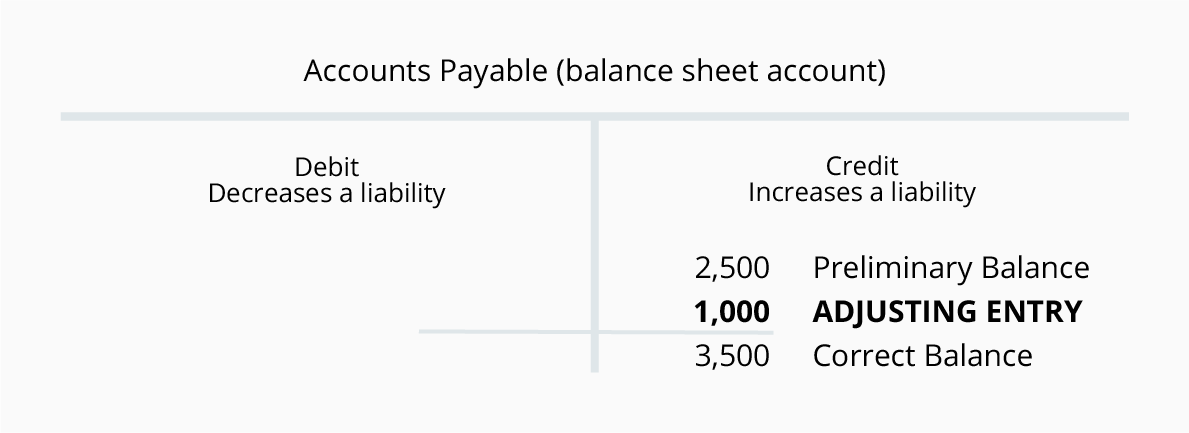

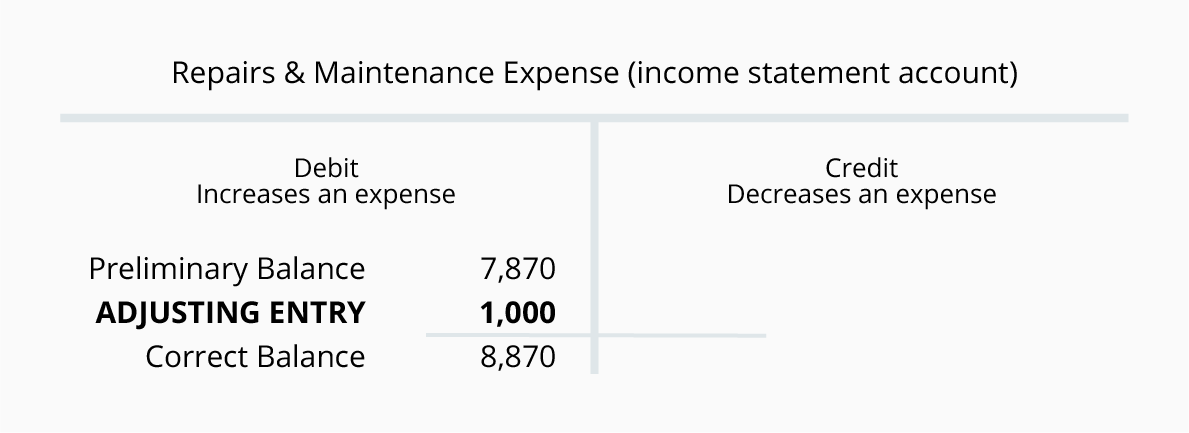

Accounts Payable $2,500

Accounts Payable is a liability account that reports the amounts owed to suppliers or vendors as of the balance sheet date. Amounts are routinely entered into this account after a company has received and verified all of the following: (1) an invoice from the supplier, (2) goods or services have been received, and (3) compared the amounts to the company's purchase order. A review of the details confirms that this account's balance of $2,500 is accurate as far as invoices received from vendors.

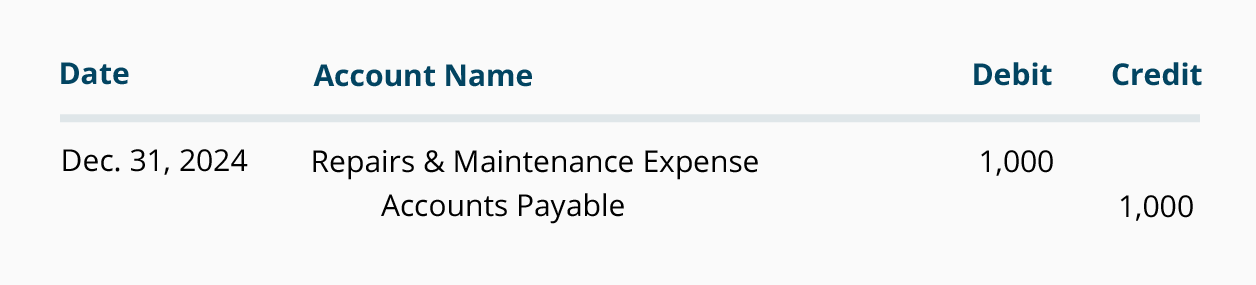

However, under the accrual basis of accounting the balance sheet must report all the amounts owed by the company—not just the amounts that have been entered into the accounting system from vendor invoices. Similarly, the income statement must report all expenses that have been incurred—not merely the expenses that have been entered from a vendor's invoice. To illustrate this, assume that a company had $1,000 of plumbing repairs done in late December, but the company has not yet received an invoice from the plumber. The company will have to make an adjusting entry to record the expense and the liability on the December financial statements. The adjusting entry will involve the following accounts:

The adjusting entry for Accounts Payable in general journal format is:

The balance in the liability account Accounts Payable at the end of the year will carry forward to the next accounting year. The balance in Repairs & Maintenance Expense at the end of the accounting year will be closed and the next accounting year will begin with $0.

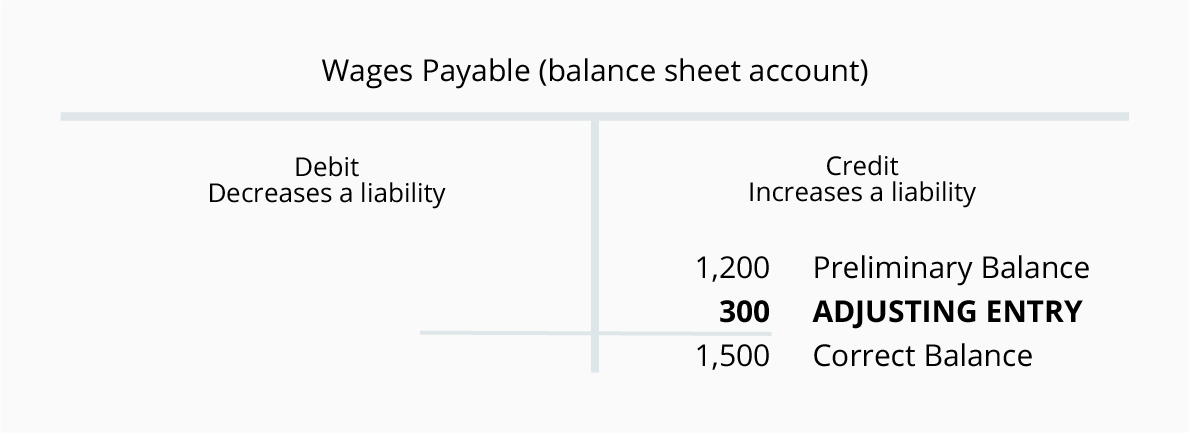

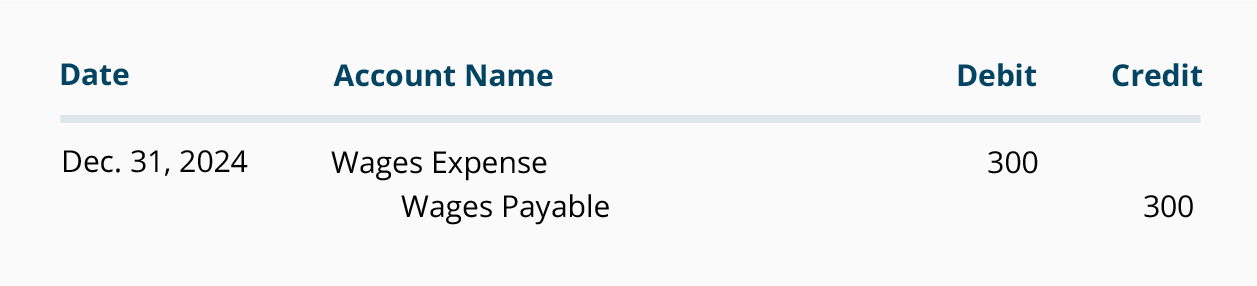

Wages Payable $1,200

Wages Payable is a liability account that reports the amounts owed to employees as of the balance sheet date. Amounts are routinely entered into this account when the company's payroll records are processed. A review of the details confirms that this account's balance of $1,200 is accurate as far as the payrolls that have been processed.

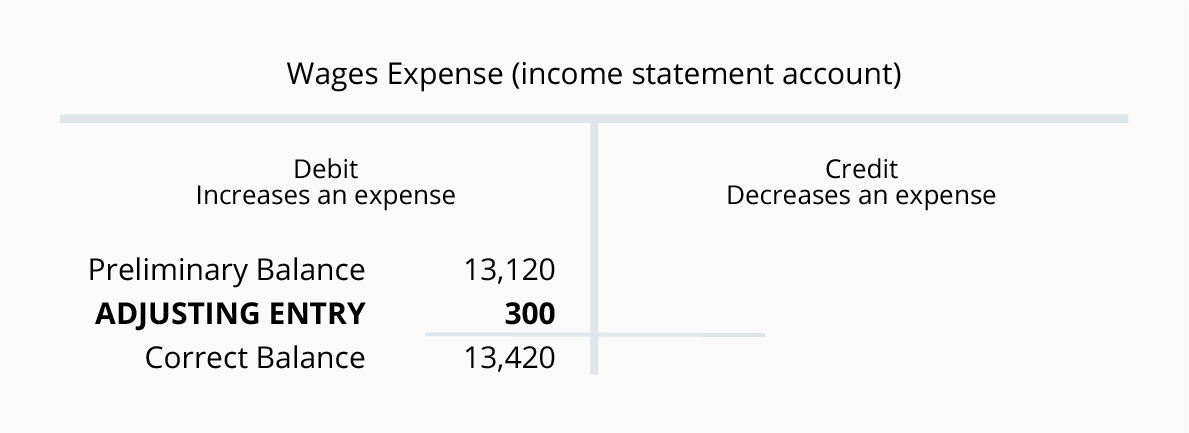

However, under the accrual basis of accounting the balance sheet must report all of the payroll amounts owed by the company—not just the amounts that have been processed. Similarly, the income statement must report all of the payroll expenses that have been incurred—not merely the expenses from the routine payroll processing. For example, assume that December 30 is a Sunday and the first day of the payroll period. The wages earned by the employees on December 30-31 will be included in the payroll processing for the week of December 30 through January 5. However, the December income statement and the December 31 balance sheet need to include the wages for December 30-31, but not the wages for January 1-5. If the wages for December 30-31 amount to $300, the following adjusting entry is required as of December 31:

The adjusting journal entry for Wages Payable is:

The $1,500 balance in Wages Payable is the true amount not yet paid to employees for their work through December 31. The $13,420 of Wages Expense is the total of the wages used by the company through December 31. The Wages Payable amount will be carried forward to the next accounting year. The Wages Expense amount will be zeroed out so that the next accounting year begins with a $0 balance.

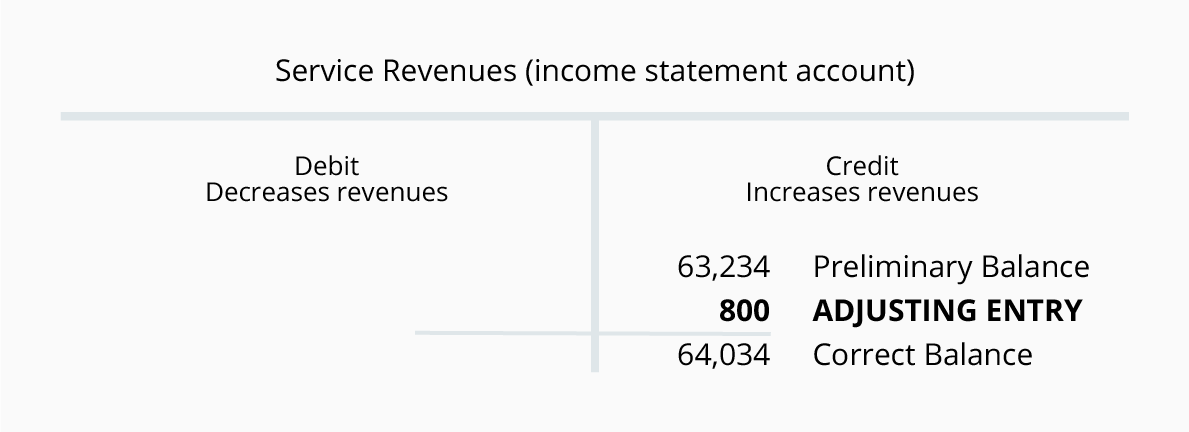

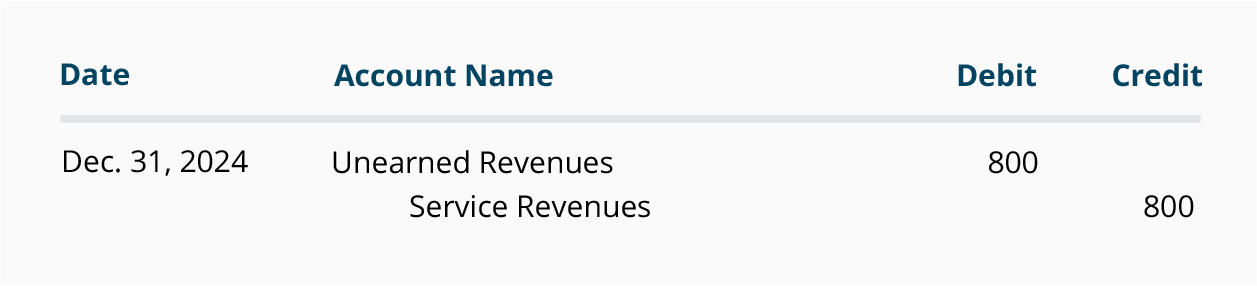

Unearned Revenues $1,300

Unearned Revenues is a liability account that reports the amounts received by a company but have not yet been earned by the company. For example, if a company required a customer with a poor credit rating to pay $1,300 before beginning any work, the company increases its asset Cash by $1,300 and it should increase its liability Unearned Revenues by $1,300.

As the company does the work, it will reduce the Unearned Revenues account balance and increase its Service Revenues account balance by the amount earned (work performed). A review of the balance in Unearned Revenues reveals that the company did indeed receive $1,300 from a customer earlier in December. However, during the month the company provided the customer with $800 of services. Therefore, at December 31 the amount of services due to the customer is $500.

Let's visualize this situation with the following T-accounts:

The adjusting entry for Unearned Revenues in general journal format is:

Since Unearned Revenues is a balance sheet account, its balance at the end of the accounting year will carry over to the next accounting year. On the other hand Service Revenues is an income statement account and its balance will be closed when the current year is over. Revenues and expenses always start the next accounting year with $0.

Accruals & Deferrals

Adjusting entries are often sorted into two groups: accruals and deferrals.

Accruals

Accruals (or accrual-type adjusting entries) involve both expenses and revenues and are associated with the first scenario mentioned in the introduction to this topic:

- Nothing has been entered in the accounting records for certain expenses and/or revenues, but those expenses and/or revenues did occur and must be included in the current period's income statement and balance sheet.

Accrual of Expenses

An accountant might say, "We need to accrue the interest expense on the bank loan." That statement is made because nothing had been recorded in the accounts for interest expense, but the company did indeed incur interest expense during the accounting period. Further, the company has a liability or obligation for the unpaid interest up to the end of the accounting period. What the accountant is saying is that an accrual-type adjusting journal entry needs to be recorded.

The accountant might also say, "We need to accrue for the wages earned by the employees on Sunday, December 30, and Monday, December 31." This means that an accrual-type adjusting entry is needed because the company incurred wages expenses on December 30-31 but nothing will be entered routinely into the accounting records by the end of the accounting period on December 31.

A third example is the accrual of utilities expense. Utilities provide the service (gas, electric, telephone) and then bill for the service they provided based on some type of metering. As a result the company will incur the utility expense before it receives a bill and before the accounting period ends. Hence, an accrual-type adjusting journal entry must be made in order to properly report the correct amount of utilities expenses on the current period's income statement and the correct amount of liabilities on the balance sheet.

Accrual of Revenues

Accountants also use the term "accrual" or state that they must "accrue" when discussing revenues that fit the first scenario. For example, an accountant might say, "We need to accrue for the interest the company has earned on its certificate of deposit." In that situation the company probably did not receive any interest nor did the company record any amounts in its accounts, but the company did indeed earn interest revenue during the accounting period. Further the company has the right to the interest earned and will need to list that as an asset on its balance sheet.

Similarly, the accountant might say, "We need to prepare an accrual-type adjusting entry for the revenues we earned by providing services on December 31, even though they will not be billed until January."

Deferrals

Deferrals or deferral-type adjusting entries can pertain to both expenses and revenues and refer to the second scenario mentioned in the introduction to this topic:

- Something has already been entered in the accounting records, but the amount needs to be divided up between two or more accounting periods.

Deferral of Expenses

An accountant might say, "We need to defer some of the insurance expense." That statement is made because the company may have paid on December 1 the entire bill for the insurance coverage for the six-month period of December 1 through May 31. However, as of December 31 only one month of the insurance is used up. Hence the cost of the remaining five months is deferred to the balance sheet account Prepaid Insurance until it is moved to Insurance Expense during the months of January through May. If the company prepares monthly financial statements, a deferral-type adjusting entry may be needed each month in order to move one-sixth of the six-month cost from the asset account Prepaid Insurance to the income statement account Insurance Expense.

The accountant might also say, "We need to defer some of the cost of supplies." This deferral is necessary because some of the supplies purchased were not used or consumed during the accounting period. An adjusting entry will be necessary to defer to the balance sheet the cost of the supplies not used, and to have only the cost of supplies actually used being reported on the income statement. The costs of the supplies not yet used are reported in the balance sheet account Supplies and the cost of the supplies used during the accounting period are reported in the income statement account Supplies Expense.

Deferral of Revenues

Deferrals also involve revenues. For example if a company receives $600 on December 1 in exchange for providing a monthly service from December 1 through May 31, the accountant should "defer" $500 of the amount to a liability account Unearned Revenues and allow $100 to be recorded as December service revenues. The $500 in Unearned Revenues will be deferred until January through May when it will be moved with a deferral-type adjusting entry from Unearned Revenues to Service Revenues at a rate of $100 per month.

Avoiding Adjusting Entries

If you want to minimize the number of adjusting journal entries, you could arrange for each period's expenses to be paid in the period in which they occur. For example, you could ask your bank to charge your company's checking account at the end of each month with the current month's interest on your company's loan from the bank. Under this arrangement December's interest expense will be paid in December, January's interest expense will be paid in January, etc. You simply record the interest payment and avoid the need for an adjusting entry. Similarly, your insurance company might automatically charge your company's checking account each month for the insurance expense that applies to just that one month.

Quiz: Take the quiz after reading.

11. An increase in value of a fixed asset is known as?

(b) Accumulated Depreciation

(c) Appreciation

(d) Written Down Value

12. Short Term Loan can be best describing as?

(b) If the period is over one year

(c) If the period is less than one year

(d) A and B

13. Which of the following is true for every adjusting entry?

(b) They affect balance sheet account and an income statement account

(c) They affect only balance sheet accounts

(d) They affect only accounts with normal debit balance

14. Unearned revenues are?

(b) Liabilities

(c) Temporary accounts

(d) Both a and b above

15. Which of the following is not an adjusting entry?

(b) Debit rent expense; credit rent payable

(c) Debit rent expense; credit pre-paid rent

(d) Debit unearned revenue; credit pre-paid expenses

16. How does failure to record accrued revenue distort the financial reports?

(b) It understates net income, stockholders’ equity, and current liabilities

(c) It overstates revenue, stockholders’ equity, and current liabilities

(d) It understates current assets and overstates stockholders’ equity

17. The purpose of adjusting entries is to?

(b) Adjust daily the balances in asset, liability, revenue and expense accounts for the effects of business transactions

(c) Apply the realization principle and the matching principle to transactions affecting two or more periods

(d) Prepare revenue and expense accounts for recording the transactions of the next accounting period

18. When the goods are provided, unearned revenue decreased and a revenue account is?

(b) Decreased

(c) Remain same

(d) A and C

19. Which of the following should not be called “Sales”?

(b) Office fixtures sold

(c) Goods sold on credit

(d) All of before

20. The revenue receipt is shown in income statement as a?

(b) Income

(c) Other income

(d) Other expense

11: C

ReplyDelete12: C

13: B

14: B

15: D

16: A

17: C

18: A

19: B

20: B

BY: Gisela Vargas Fuentes.

11). C

ReplyDelete12). C

13). B

14). B

15). D

16). A

17). C

18). A

19). B

20). B

By: Damaris Ivonn Alvites Vasquez

11) An increase in value of a fixed asset is known as?

ReplyDelete-c

12) Short Term Loan can be best describing as?

-c

13) Which of the following is true for every adjusting entry?

-b

14) Unearned revenues are?

-b

15) Which of the following is not an adjusting entry?

-d

16) How does failure to record accrued revenue distort the financial reports?

-a

17) The purpose of adjusting entries is to?

-c

18) When the goods are provided, unearned revenue decreased and a revenue account is?

-a

19) Which of the following should not be called “Sales”?

-b

20) The revenue receipt is shown in income statement as a?

-b

(BY: Jose rafael-)

11) C

ReplyDelete12) C

13) B

14) B

15) D

16) A

17) C

18) A

19) B

20) B

BY: FARID PINEDO

11.- c

ReplyDelete12.- c

13.- b

14.- b

15.- d

16.- a

17.- c

18.- a

19.- b

20.- b

By: Felix

By: Jesús Huaman

ReplyDelete11) c

12) c

13) b

14) b

15) d

16) a

17) c

18) a

19) b

20) b

11: (C)

ReplyDelete12: (C)

13: (B)

14: (B)

15: (D)

16: (A)

17: (C)

18: (A)

19: (B)

20: (B)

By(Fiorela Mendez)

11): C

ReplyDelete12): C

13): B

14): B

15): D

16): A

17): C

18): A

19): B

20): B

By: jeff echevarria

11. (c) Appreciation

ReplyDelete12. (c) If the period is less than one year

13. (b) They affect balance sheet account and an income statement account

14. (b) Liabilities

15. (d) Debit unearned revenue; credit pre-paid expenses

16. (a) It understates revenue, net income, and current assets

17.(c) Apply the realization principle and the matching principle to transactions affecting two or more periods

18. (a) Increased

19. (b) Office fixtures sold

20. (b) Income

11): C

ReplyDelete12): C

13): B

14): B

15): D

16): A

17): C

18): A

19): B

20): B

by: cristian calle

11.(c)

ReplyDelete12.(c)

13.(b)

14.(b)

15.(d)

16.(a)

17.(c)

18.(a)

19.(b)

20.(b)

BY :YENI PEREZ

11- C

ReplyDelete12-C

13-B

14-B

15-D

16-A

17-C

18-A

19-B

20-B

Ary Ganoza Torres

11: C

ReplyDelete12: C

13: B

14: B

15: D

16: A

17: C

18: A

19: B

20: B

By: (Keisy Mylene López Vásquez)

11. C

ReplyDelete12. C

13. B

14. B

15. D

16. A

17. C

18. A

19. B

20. B

BY: DEANELLI JULCA

11) C

ReplyDelete12) C

13) B

14) B

15) D

16) A

17) C

18) A

19) B

20) B

BY: Paola Aguilar

11. C

ReplyDelete12. C

13. B

14. B

15. D

16. A

17. C

18. A

19. B

20. B

By Rocio Sanchez

11.- C

ReplyDelete12.-C

13.-B

14.-B

15.-D

16.-A

17.-C

18.-A

19.-B

20.-B

By Widman

11) C

ReplyDelete12) C

13) B

14) B

15) D

16) A

17) C

18) A

19) B

20) B

BY: MAGDIEL

11. c

ReplyDelete12. c

13. b

14. b

15. d

16. a

17. c

18. a

19. b

20. b

This comment has been removed by the author.

ReplyDelete11. C

ReplyDelete12. C

13. B

14. B

15. D

16. A

17. C

18. A

19. B

20. B

by: Ruth Chanchari

11= C

ReplyDelete12= C

13= B

14= B

15= D

16= A

17= C

18= A

19= B

20=B

By:Lily Carrasco

14.Unearned revenues are?

ReplyDelete(b) Liabilities

15.Which of the following is not an adjusting entry?

(d) Debit unearned revenue; credit pre-paid expenses

16.How does failure to record accrued revenue distort the financial reports?

(a) It understates revenue, net income, and current assets

17.The purpose of adjusting entries is to?

(c) Apply the realization principle and the matching principle to transactions affecting two or more periods

18.When the goods are provided, unearned revenue decreased and a revenue account is?

(a) Increased

19.Which of the following should not be called “Sales”?

(b) Office fixtures sold

20. The revenue receipt is shown in income statement as a?

(b) Income

BY(juanita tocas)

11. C) Appreciation.

ReplyDelete12. C) If the period is less than one year.

13. B) They affect balance sheet account and an income statement account.

14. B) Liabilities.

15. D) Debit unearned revenue; credit pre-paid expenses.

16. A) It understates revenue, net income, and current assets.

17. C) Apply the realization principle and the matching principle to transactions affecting two or more periods.

18. A) Increased.

19. B) Office fixtures sold.

20. B) Income.

BY. Noli Cubas

11.- (c)

ReplyDelete12.- (c)

13.- ( b)

14.- (b)

15.- (d)

16.- (a)

17.- (c)

18.- (a)

19.- (b)

20.- (b)

by giovany castillo

11. C) Appreciation.

ReplyDelete12. C) If the period is less than one year.

13. B) They affect balance sheet account and an income statement account.

14. B) Liabilities.

15. D) Debit unearned revenue; credit pre-paid expenses.

16. A) It understates revenue, net income, and current assets.

17. C) Apply the realization principle and the matching principle to transactions affecting two or more periods.

18. A) Increased.

19. B) Office fixtures sold.

20. B) Income.

By. Frank Tantarico

By: Alessandro G.

ReplyDelete11_. C

12_. C

13_: B

14_. B

15_. D

16_. A

17_. C

18_. A

19_. B

20_. B

11-c

ReplyDelete12-c

13-b

14-a

15-d

16-d

17-a

18-d

19-c

20-b

merli cotrina

11) C

ReplyDelete12) C

13) B

14) B

15) D

16) A

17) C

18) A

19) B

20) B