Cash flow statement 2

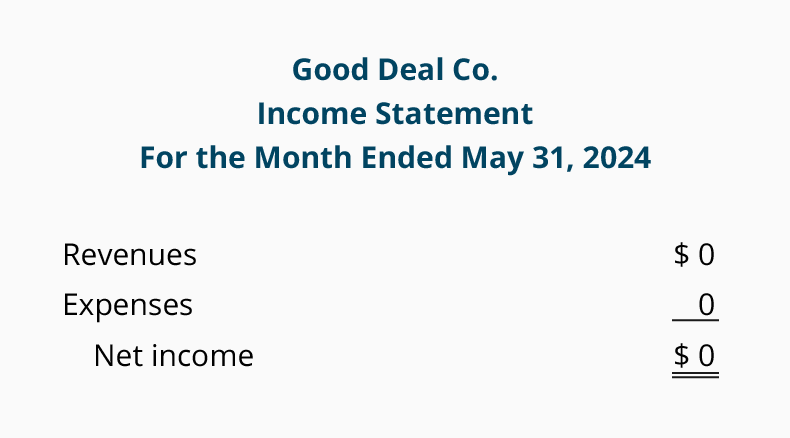

May Transactions and Financial Statements

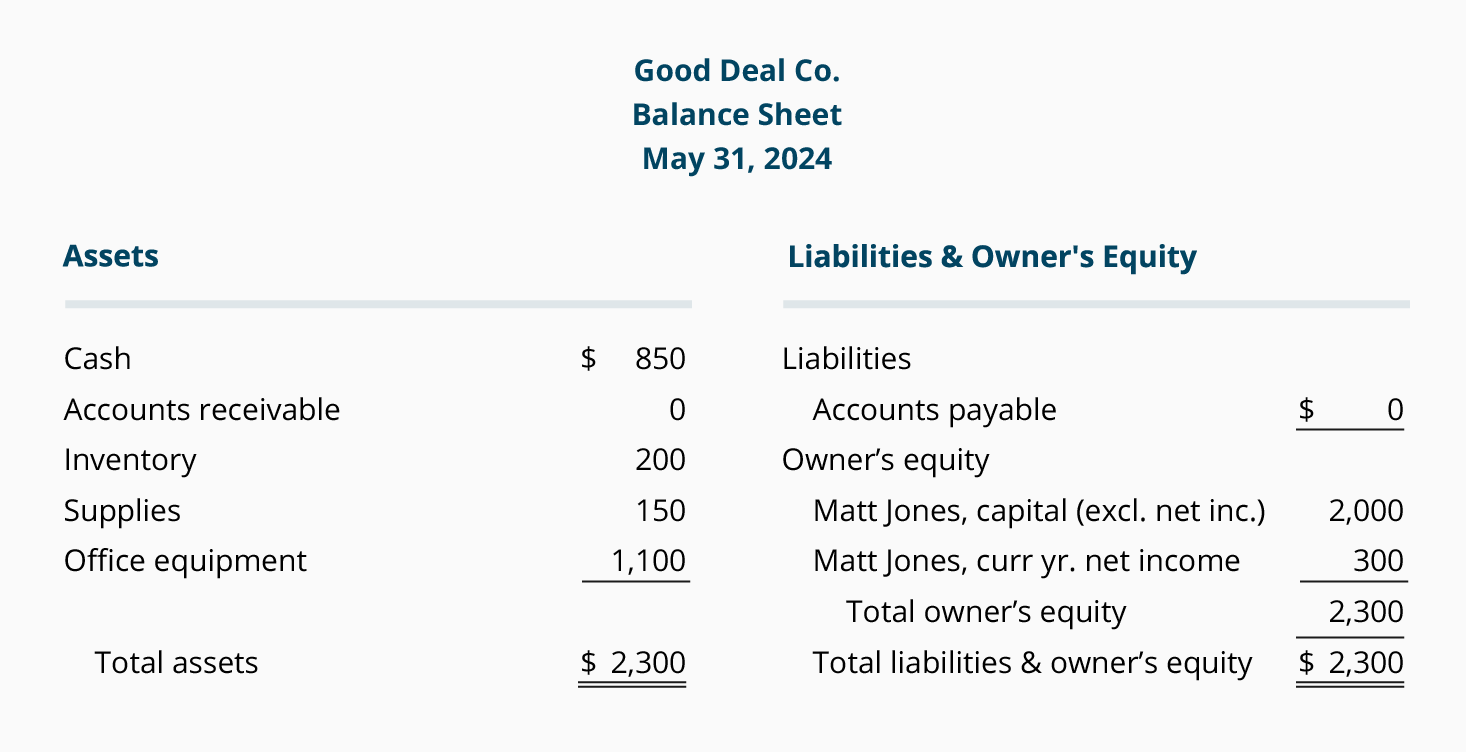

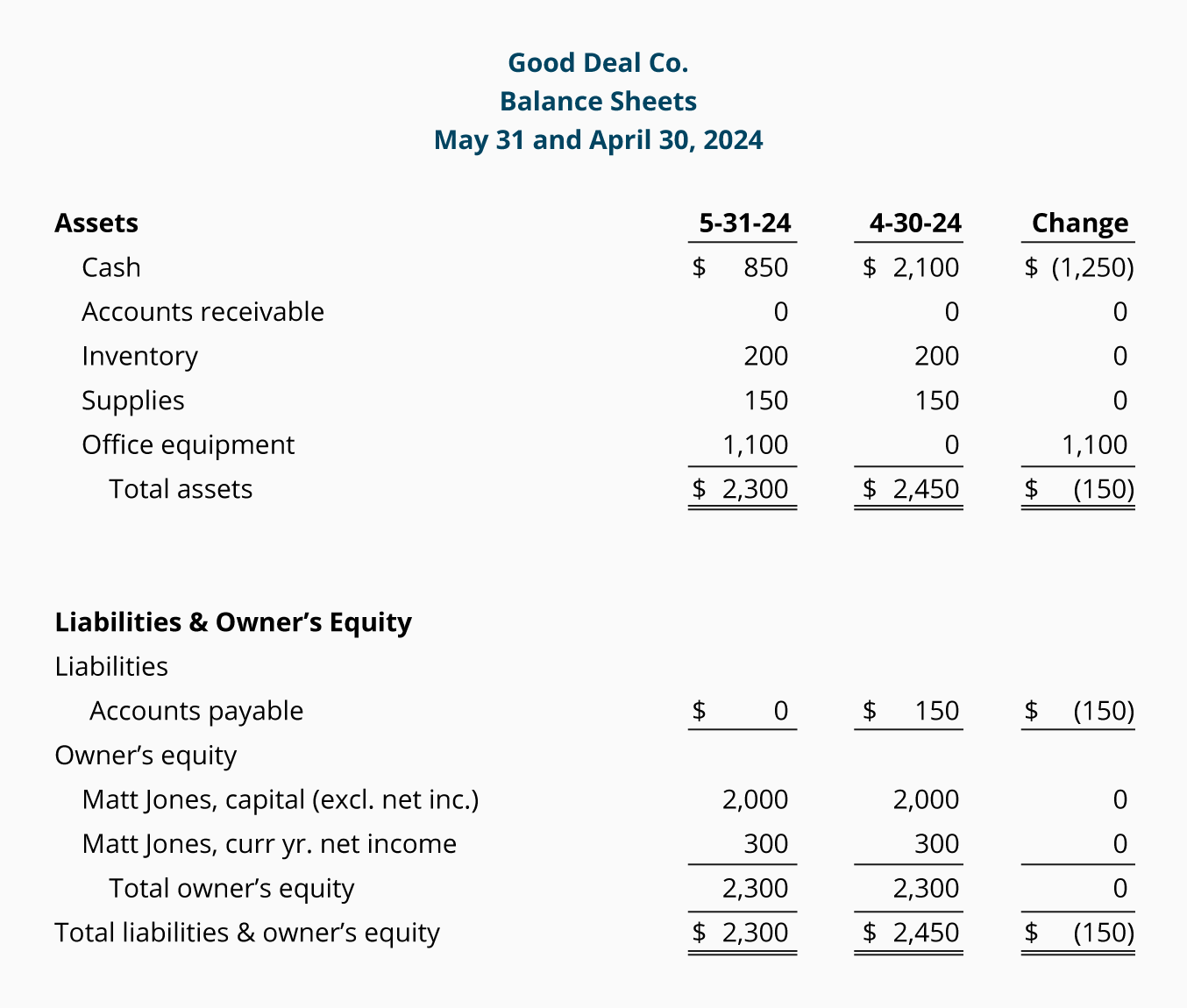

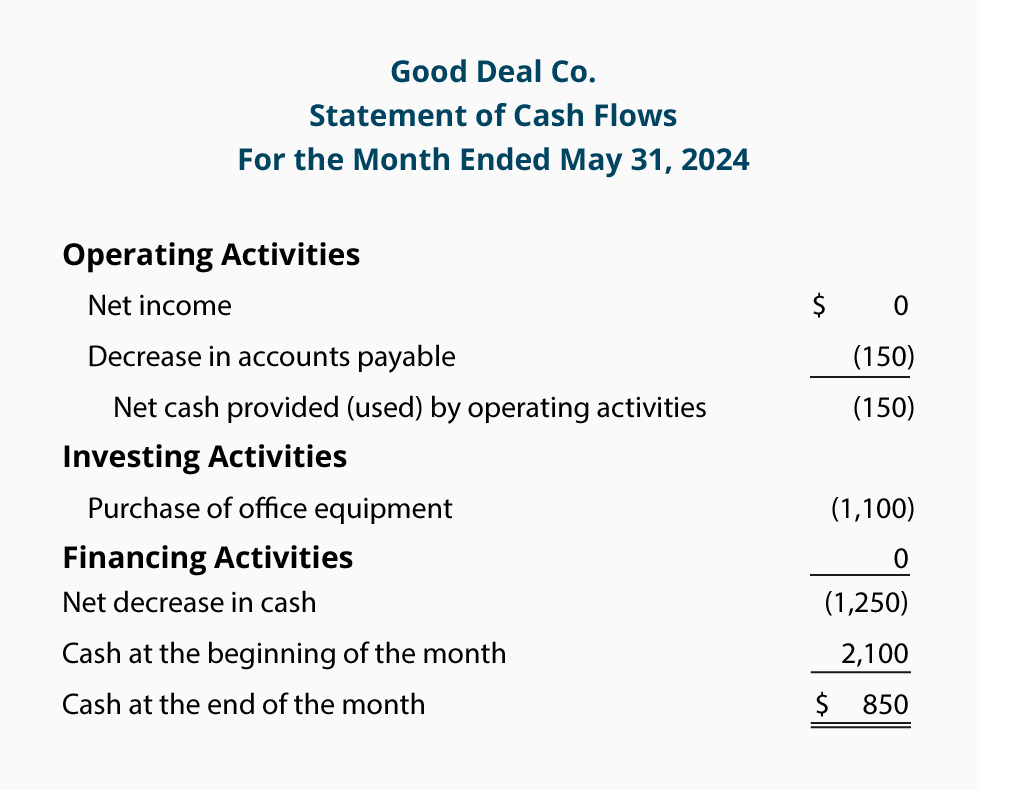

On May 30 Good Deal pays its accounts payable of $150. On May 31 Good Deal purchases office equipment (a new computer and printer) that will be used exclusively in the business. The cost of the office equipment is $1,100 and is paid in cash. There were no other transactions in May.

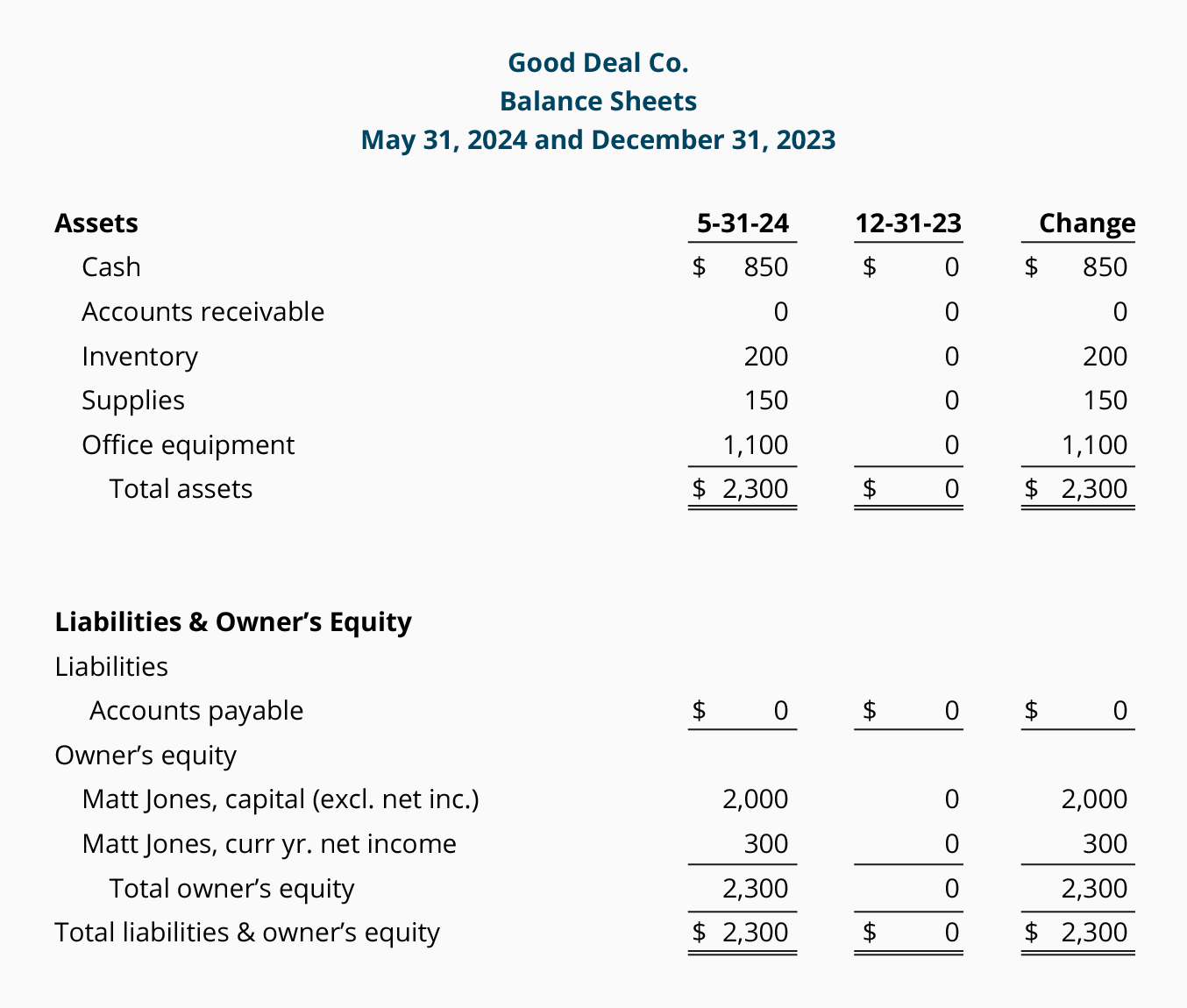

A balance sheet comparing May 31 amounts to April 30 amounts and the resulting differences or changes is shown here:

The following comparative balance sheet shows the changes between December 31, 2019 and May 31, 2020:

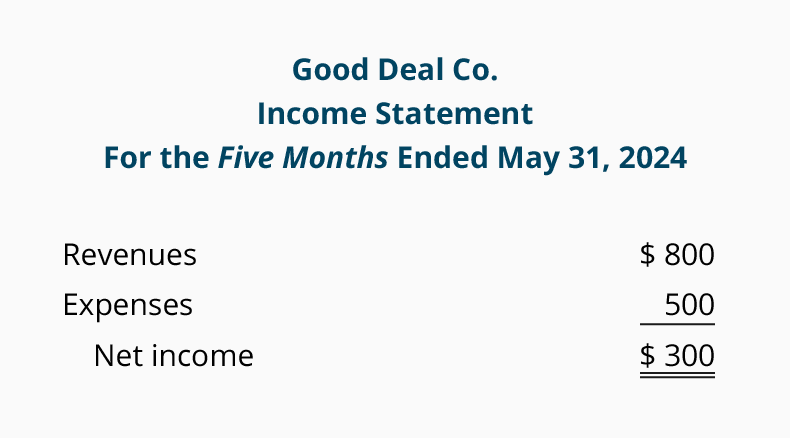

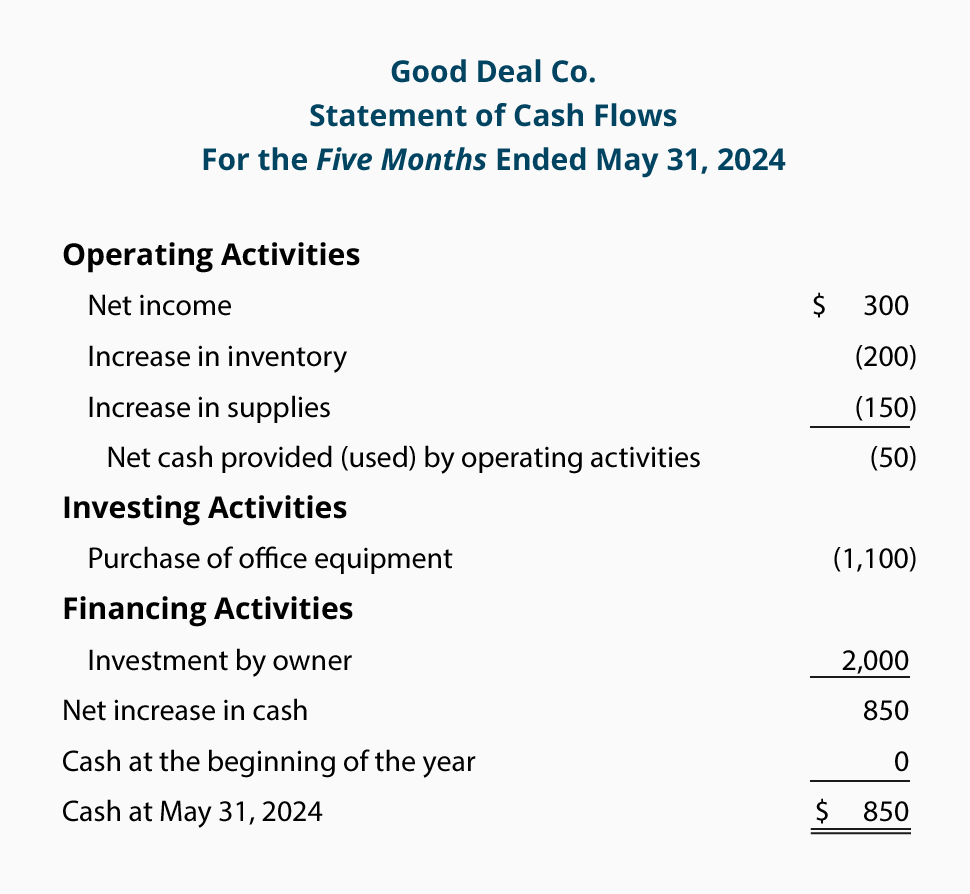

The SCF for the period of January 1 through May 31 is:

Let's review the cash flow statement for the five months ended May 31:

The operating activities section starts with the net income of $300 for the five-month period. The increase in Inventory was not good for cash, as shown by the negative adjustment of $200. Similarly, the increase in Supplies was not good for cash and it is reported as a negative adjustment of $150. Combining the amounts, the net change in cash that is explained by operating activities is a negative $50.

The investing activities section reports the increase in long-term assets as (1,100) since it was a cash outflow of $1,100. The additions to property, plant and equipment are frequently described as capital expenditures.

There were no changes in short-term loans payable or long-term liabilities. However, there was a change in owner's equity since December 31. As a result, the financing activities section of the SCF reports the owner's investment of $2,000, which increased Good Deal's cash balance.

Combining the amounts from the operating, investing, and financing activities, the SCF reports an increase in cash of $850. This agrees with the change in the Cash amounts reported on the balance sheets dated December 31, 2019 and May 31, 2020.

Depreciation Expense

Depreciation moves the cost of an asset from the balance sheet to Depreciation Expense on the income statement in a systematic manner during an asset's useful life. The accounts involved in recording depreciation are Depreciation Expense and Accumulated Depreciation. As you see, cash is not involved. In other words, depreciation reduces net income on the income statement, but it does not reduce the company's cash that is reported on the balance sheet.

Since we begin the statement of cash flows with the net income figure taken from the income statement, we need to adjust the amount of net income by adding back the amount of the Depreciation Expense.

Depletion Expense and Amortization Expense are accounts similar to Depreciation Expense. They involve allocating the cost of a long-term asset to an expense over the useful life of the asset, but no cash is involved.

Here's a Tip

In the operating activities section of the cash flow statement, add back expenses that did not require the use of cash. Examples are depreciation, depletion, and amortization expense.

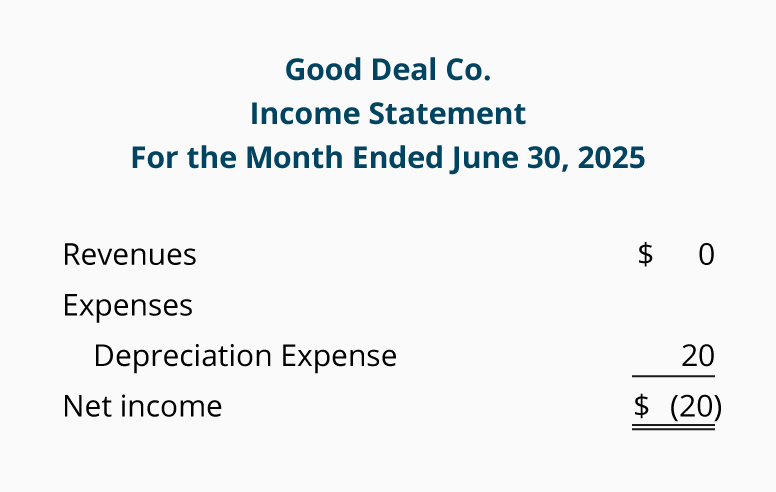

Next, we examine how depreciation expense is reported on the Good Deal Co.'s financial statement.

June Transactions and Financial Statements

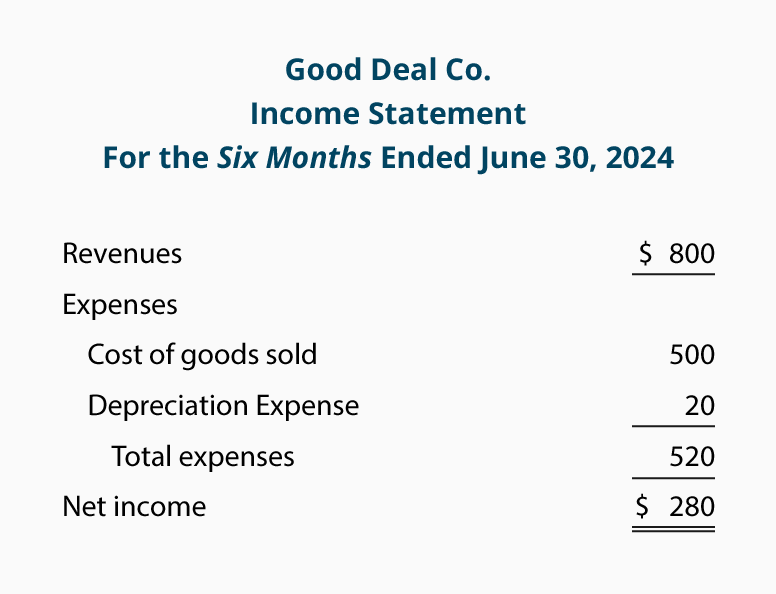

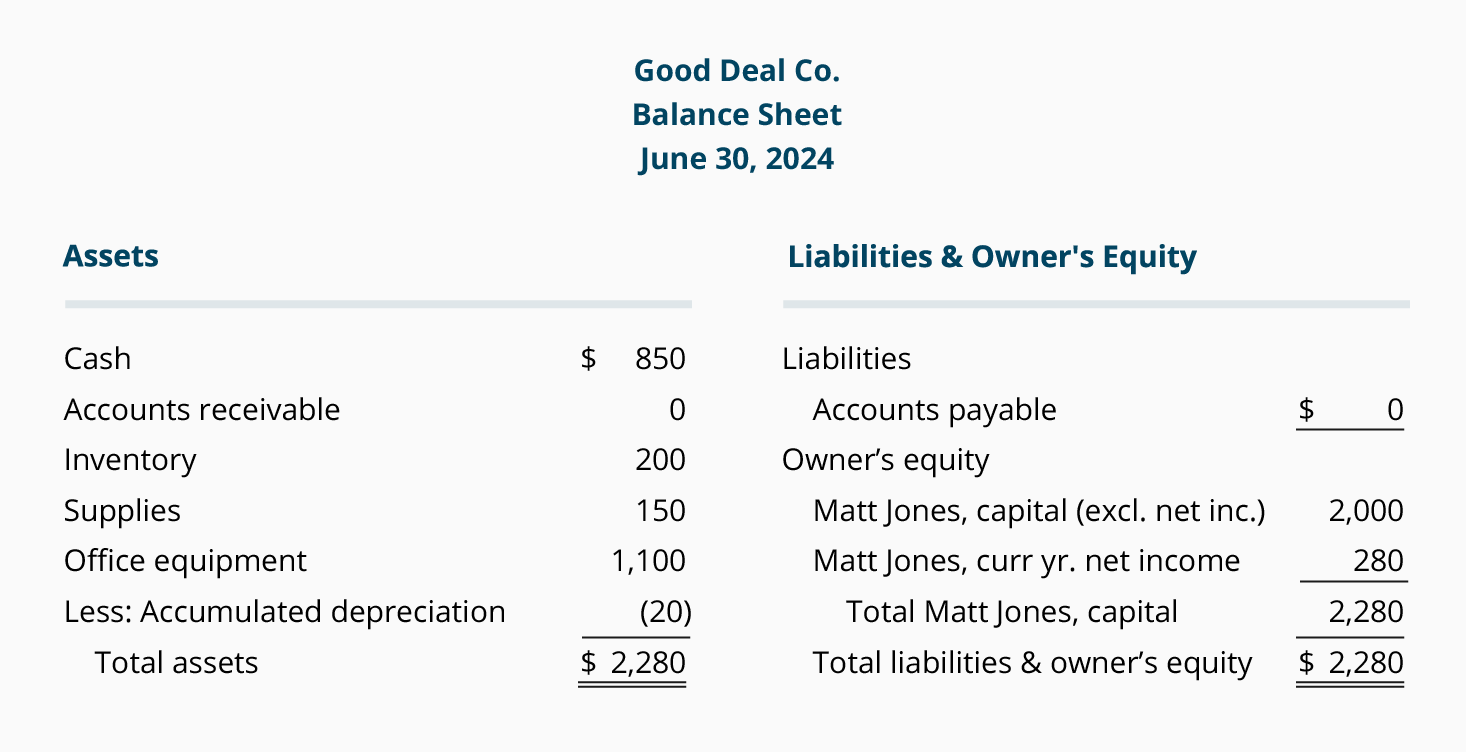

The only transaction recorded by Good Deal during June was the depreciation of its office equipment. Recall that on May 31 Good Deal purchased the office equipment (a new computer and printer) for $1,100 and it was put into service on the next day. Let's assume that depreciation expense of $20 per month is recorded by Good Deal. As a result, Good Deal's financial statements at June 30 will be as follows:

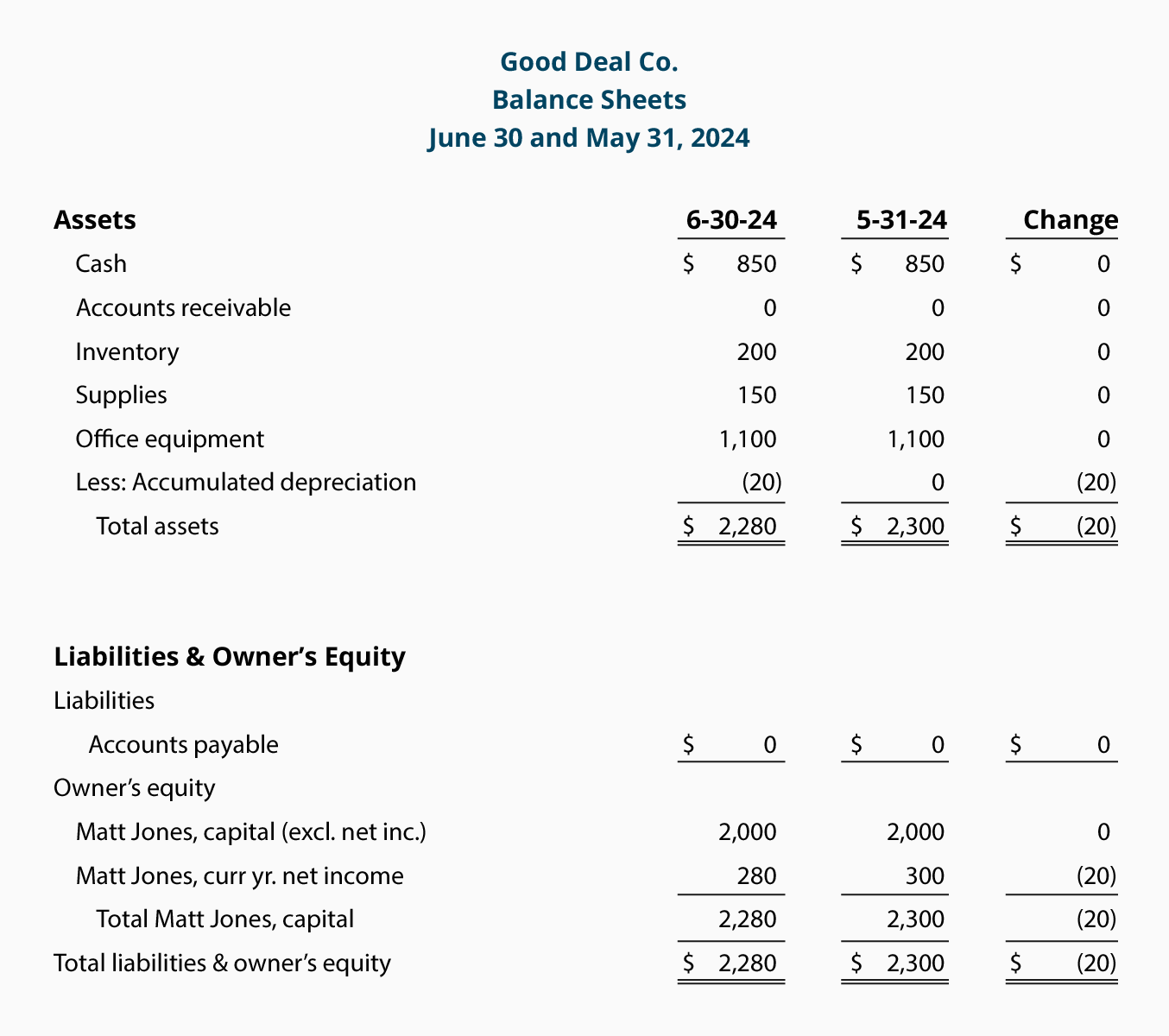

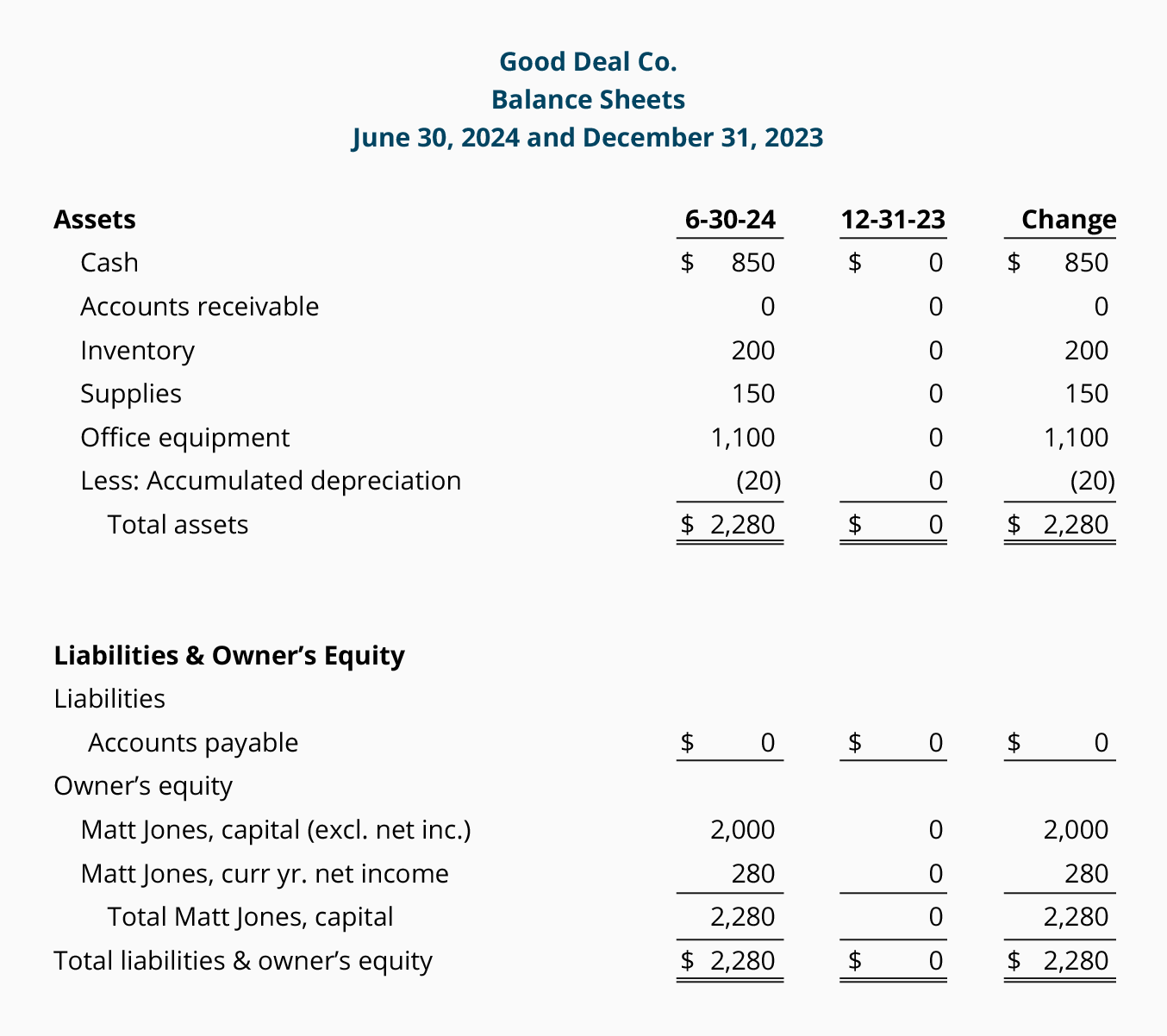

A balance sheet comparing June 30 amounts to May 31 amounts and the resulting differences or changes is shown here:

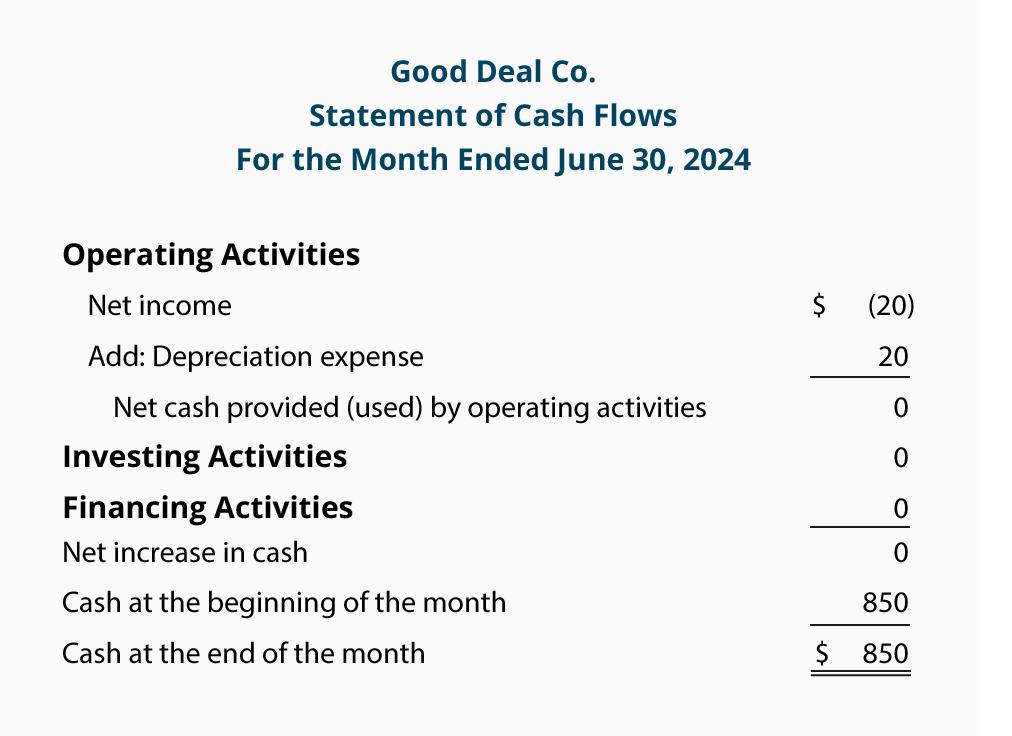

The cash flow statement for the month of June illustrates why depreciation expense needs to be added back to net income. Good Deal did not spend any cash in June, however, the entry in the Depreciation Expense account resulted in a net loss on the income statement. On the SCF, we convert the bottom line of the income statement for the month of June (a loss of $20) to the net amount of cash provided or used by operating activities, which was $0. This is done with a positive adjustment which adds back the $20 of depreciation expense.

The following comparative balance sheet shows the changes between December 31, 2019 and June 30, 2020:

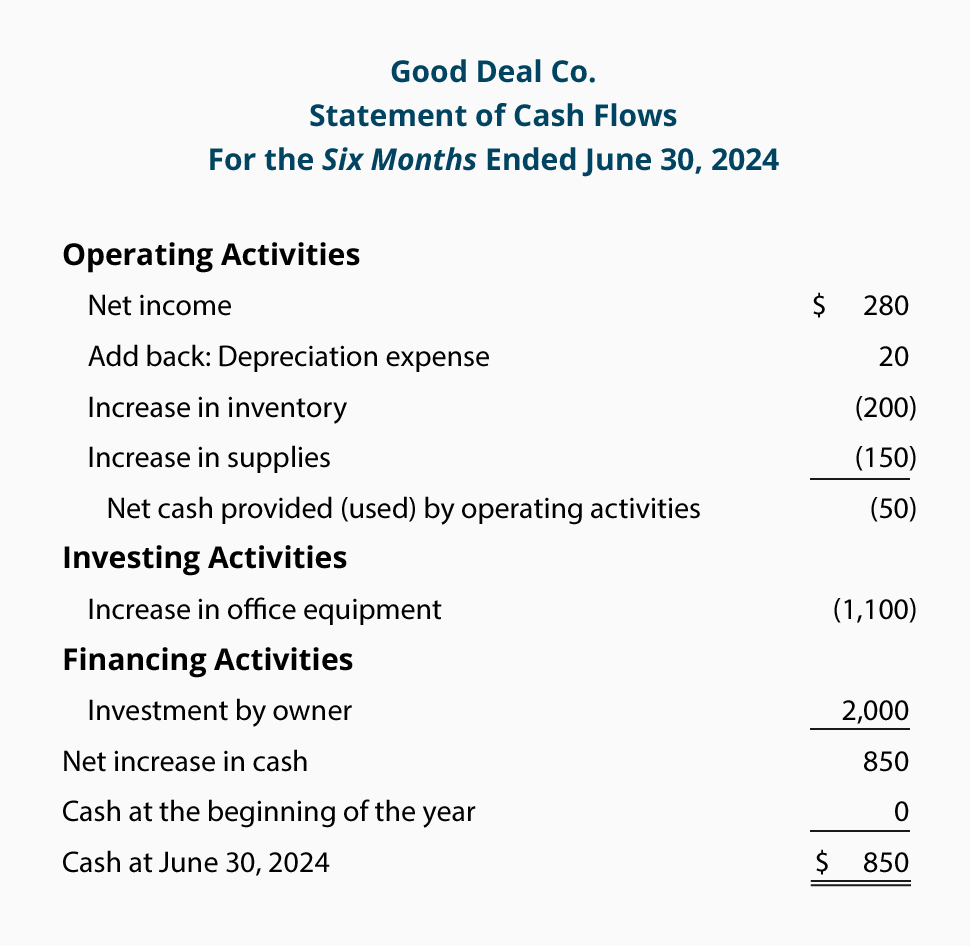

The SCF for the period of January 1 through June 30 is:

Let's review the cash flow statement for the six months ended June 30:

The operating activities section began with the net income of $280 for the six-month period. Depreciation expense is added back to net income because it was a noncash transaction (net income was reduced, but there was no cash outflow for depreciation). The increase in the Inventory account was not good for cash, as shown by the negative $200. Similarly, the increase in Supplies was not good for cash and it is reported as a negative $150. Combining the amounts, the net change in cash that is explained by operating activities is a negative $50.

The investing activities section reports the cash outflow of $1,100 for the purchase of office equipment.

There were no changes in short-term loans payable or long-term liabilities. However, there was the owner's $2,000 investment in the Good Deal Co. Therefore, the financing activities section reports a positive 2,000.

Combining the amounts from the operating, investing, and financing activities, the SCF reports an increase in cash of $850. This agrees with the change in the Cash amounts reported on the balance sheets dated December 31, 2019 and June 30, 2020.

Disposal of Assets

If a company disposes of (sells) a long-term asset for an amount different from the amount in the company's accounting records (the asset's book value), an adjustment must be made to the amount of net income appearing as the first item on the SCF.

To illustrate, assume a company sells one of its delivery trucks for $3,000. The truck is in the accounting records at its original cost of $20,000. Its accumulated depreciation is $18,000. Combining the $20,000 and the $18,000 results in a book value (or carrying value) of $2,000.

Because the cash received/proceeds from the sale of the truck was $3,000 and the book value was $2,000 the difference of $1,000 is reported as a gain on the income statement. As a result, the company's net income will increase by $1,000. (If the truck had sold for $1,500 there would be a $500 loss, which would reduce the company's net income.)

One of the rules in preparing the SCF is that the entire proceeds received from the sale of a long-term asset must be reported in the section of the SCF entitled investing activities. This presents a problem because any gain or loss on the sale of an asset is included in the amount of net income shown in the SCF section operating activities. To overcome this problem, each gain is deducted from the net income and each loss is added to the net income in the operating activities section of the SCF.

We will demonstrate the loss on the disposal of an asset in Good Deal's next transaction.

July Transactions and Financial Statements

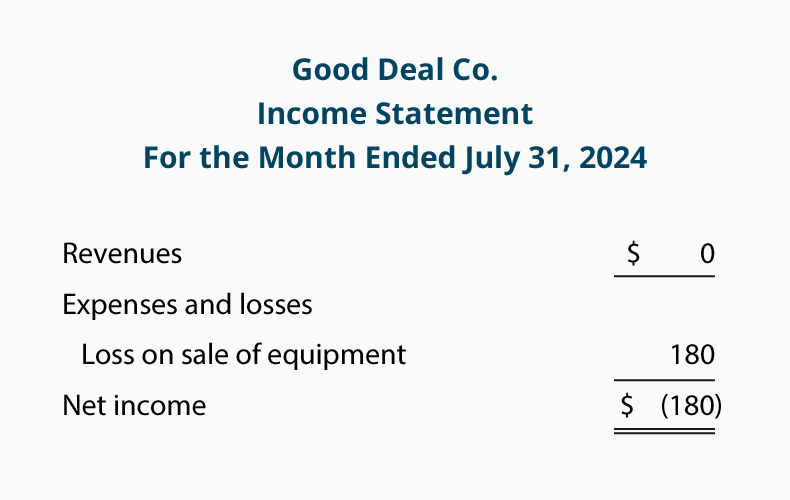

On July 1, Matt decides that his company no longer needs its office equipment. Good Deal used the equipment for one month (June 1 through June 30) and had recorded one month's depreciation of $20. This means the book value of the equipment is $1,080 (the original cost of $1,100 less the $20 of accumulated depreciation). On July 1, Good Deal sells the equipment for $900 in cash and reports the resulting $180 loss on sale of equipment on its income statement. There were no other transactions in July.

The income statement for the month of July will show how the disposal of the equipment is reported:

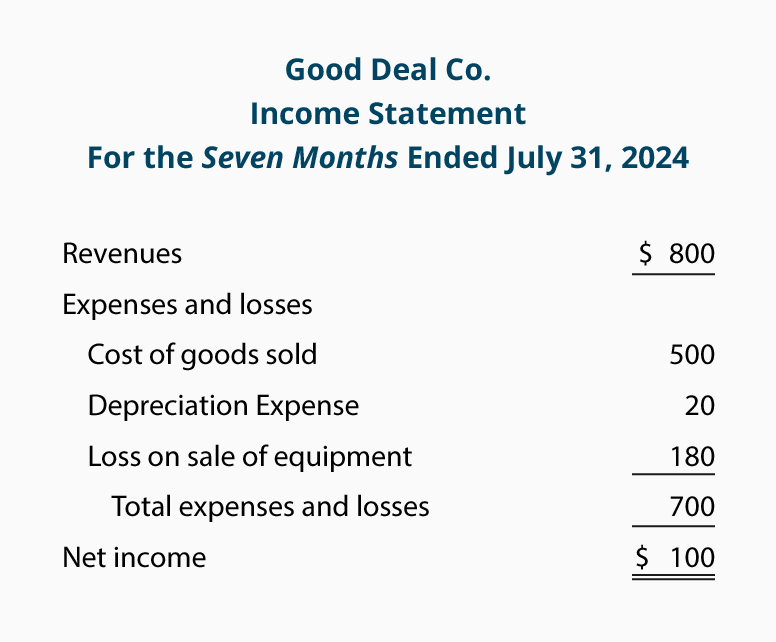

The income statement for the period of January 1 through July 31 is:

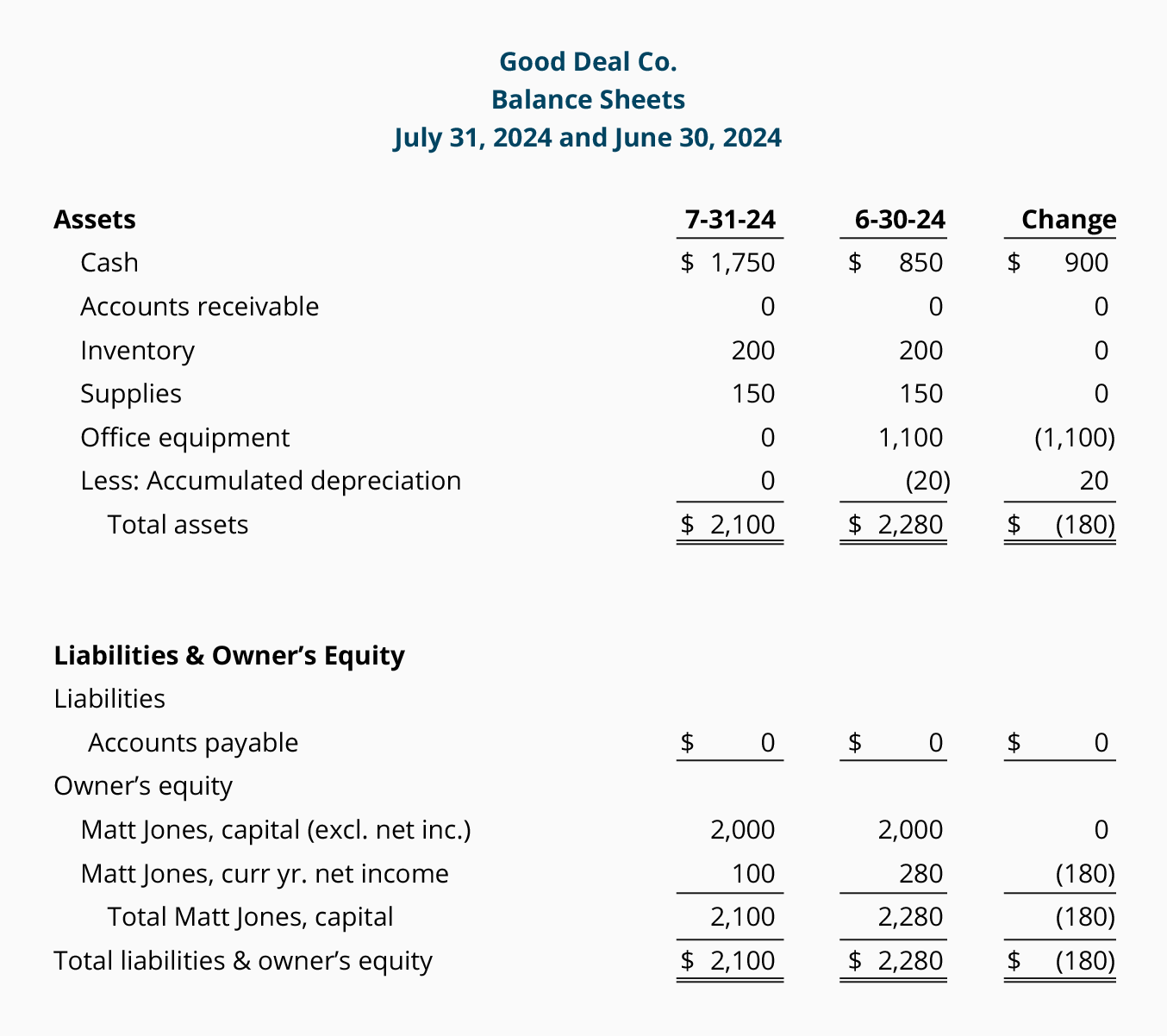

The following comparative balance sheet shows the changes that occurred during July:

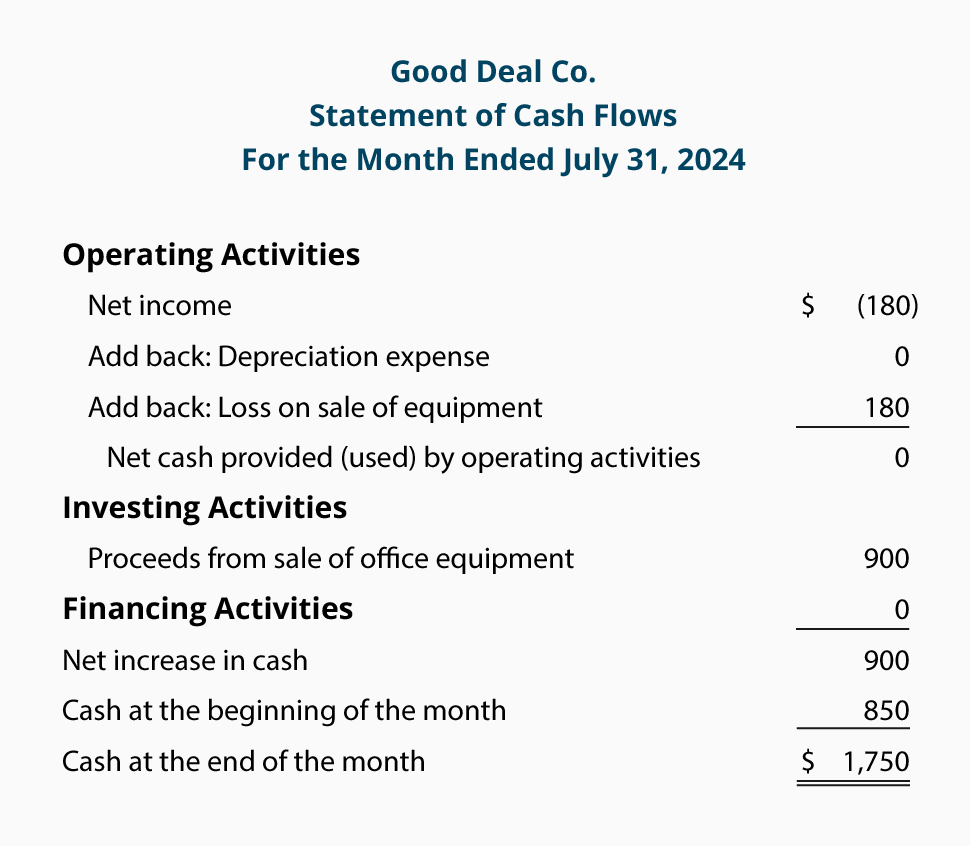

The SCF for the one month of July is:

Let's review the cash flow statement for the month of July 2020:

Net income for July was a net loss of $180. There were no revenues, expenses, or gains, but there was a loss of $180 on the sale of equipment. However, the loss did not cause the company's cash to decrease. The $900 of cash that was received is shown under investing activities.

There was no depreciation expense in July because the asset was sold on July 1. (We could have omitted the line "Depreciation Expense".) Also, the current assets and current liabilities did not change in July.

The net amount of cash provided or used by operating activities during the month of July was $0.

The investing activities section reports the $900 received from the sale of its office equipment.

There was no change in short-term loans payable, long-term liabilities, or owner's equity during July (other than the $180 loss on sale of equipment).

The sum of the amounts on the SCF for the month of July was a positive cash inflow of $900. This amount agrees to the increase in the company's cash balance from June 30 to July 31.

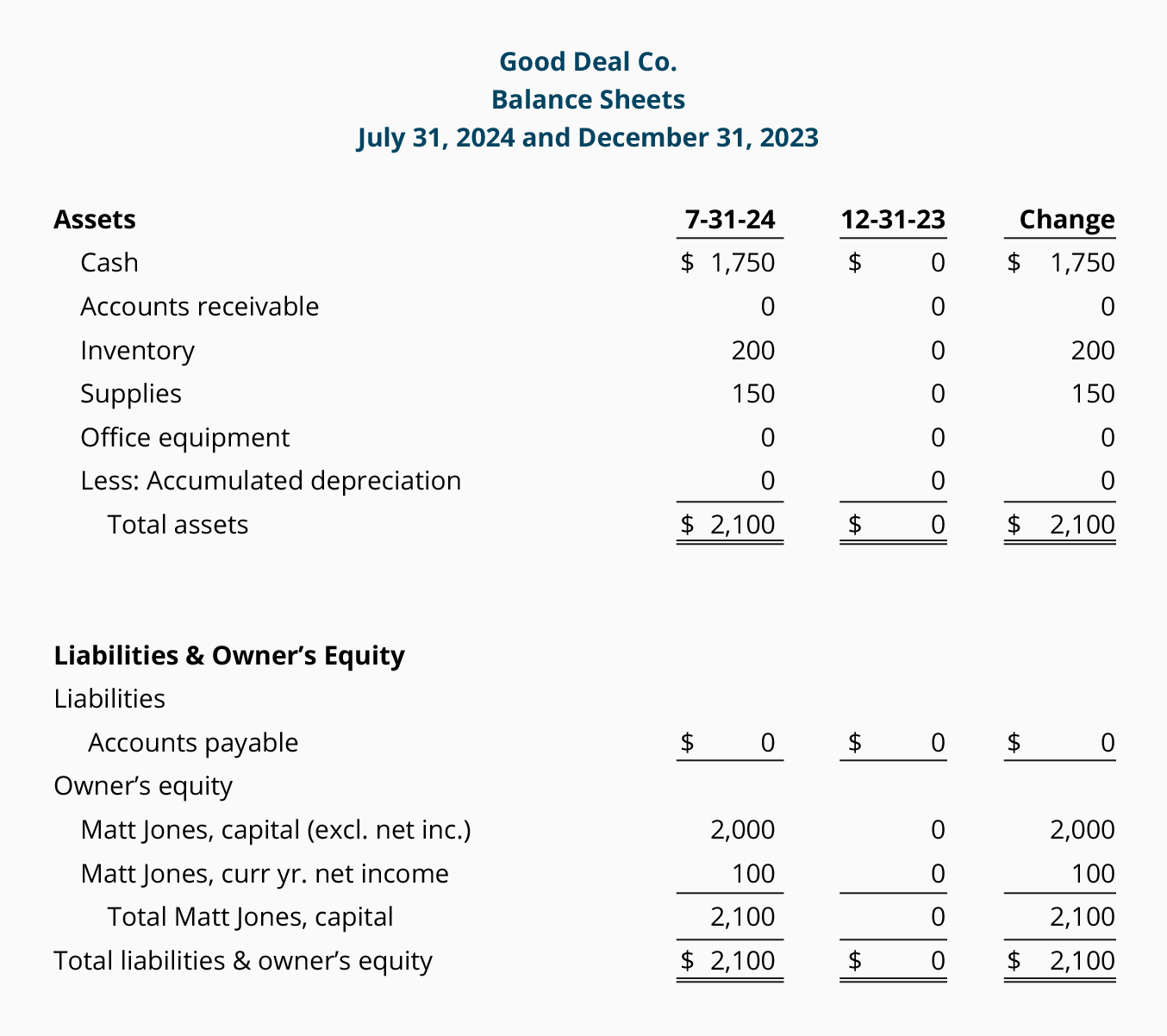

The following comparative balance sheet shows the changes between December 31, 2019 and July 31, 2020:

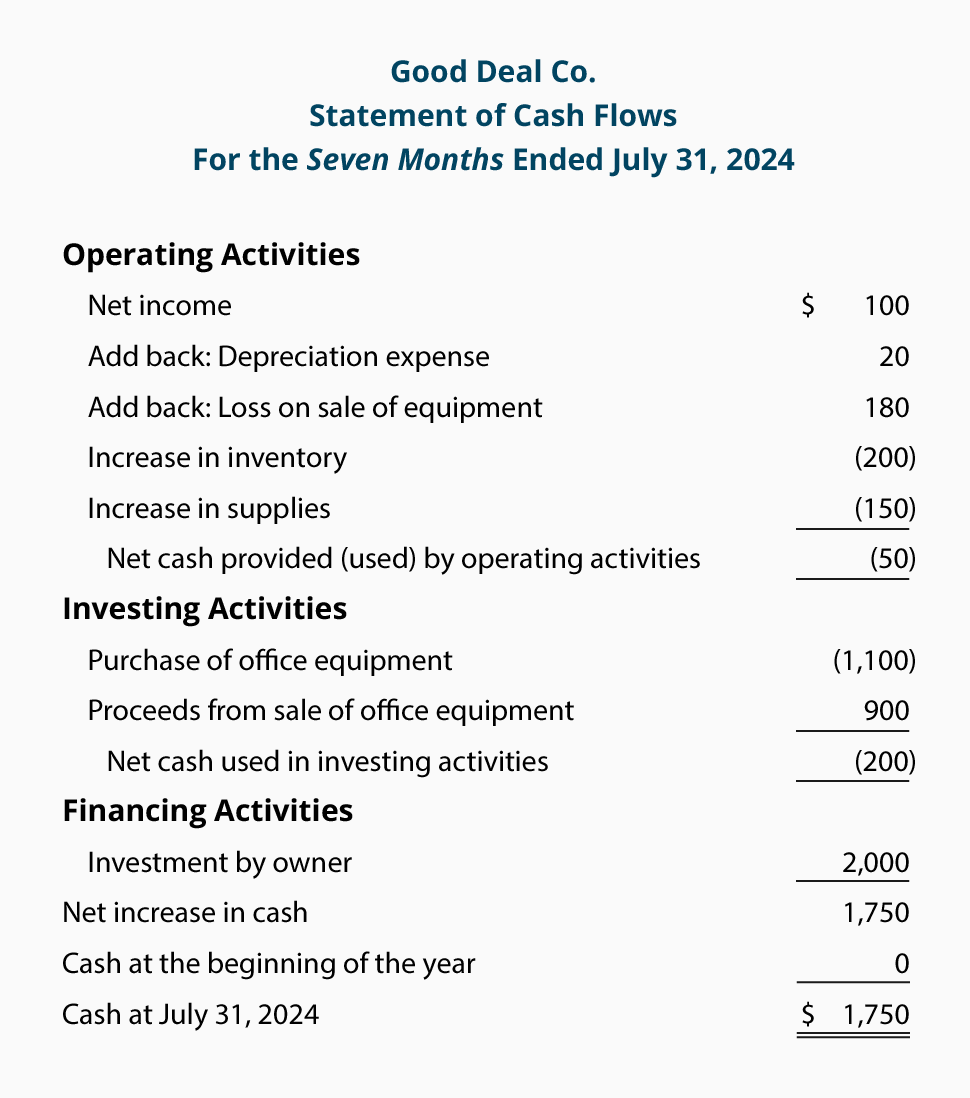

The SCF for the period of January 1 through July 31 is:

Let's review the cash flow statement for the seven months of January through July 2020:

Net income for the seven months was $100. This includes the company's revenues, gains, expenses, and losses.

Included in the net income for the seven months is $20 of depreciation expense. This expense reduced net income but did not reduce the Cash account. Therefore, the $20 of depreciation expense is a positive adjustment to the $100 of net income.

Also included in the net income was the $180 loss on sale of equipment. This loss was reported on the income statement thereby reducing net income. However, cash was not reduced. Actually, cash of $900 was received from the sale of the equipment and it is reported in its entirety in the investing activities section of the SCF.

Inventory on July 31 is $200 (4 calculators at a cost of $50 each). Since the company began with no inventory, this increase in the Inventory account means that $200 of cash was used to increase inventory. Hence, the adjustment is shown in parentheses.

Supplies increased from none to $150. The increase in the Supplies account is assumed to have had a negative effect of $150 on the company's cash.

Combining the amounts so far, we see that the net amount of cash from operating activities is a negative $50. In other words, rather than providing cash, the operating activities used a net $50 of cash.

There is cash outflow (or payment) of $1,100 to purchase the office equipment on May 31. On July 1, there was also a $900 cash inflow (or receipt) from the sale of the office equipment. Combining these two amounts results in the net outflow of $200 in the investing activities section as a source of cash.

The owner's investment of $2,000 made on January 2 is reported in the financing activities section.

Net increase in cash during the seven months was a positive $1,750 (the combination of the totals of the three sections—operating, investing, and financing activities). This $1,750 agrees to the check figure—the increase in the cash from the beginning of January to July 31.

Understanding the Indirect Method for a Cash Flow Statement

At the end of each accounting period, companies prepare financial statements showing how much money they have made or spent. The indirect method for a cash flow statement is a popular way to do this. You might need to know how to prepare an indirect method statement of cash flows if you work in a company's accounting or finance department. In this article, we explain how to create a cash flow statement using the indirect method and provide an example to follow.

What is the indirect method for a cash flow statement?

The indirect method for a cash flow statement is a way to present data that shows how much money a company spent or made during a certain period and from what sources. It takes the company's net income and adds or deducts balance sheet items to determine cash flow. Cash flow statements include three sections:

- Operating activities, such as sales of products or services, supplies or materials bought, business expenses and employee salaries

- Investing activities, such as assets bought or sold and loans paid or collected

- Financing activities, such as those involving stocks, bonds or dividends

Business owners, investors, creditors and stakeholders monitor cash flow statements to assess a company's performance. An organization might prepare cash flow statements monthly, quarterly and/or annually.

The other way to prepare a cash flow statement is using the direct method, which does not start its calculations from the company's net income and factors cash payments and receipts into the total balance. The direct method is based on cash accounting, while the indirect method is based on accrual accounting, which involves reporting income for the period in which it was earned rather than received. Both methods get the same result, but many accountants prefer the indirect method because they can prepare it more easily using information from existing financial documents.

How to prepare a cash flow statement using the indirect method

When preparing a cash flow statement using the indirect method, follow these steps:

Gather the necessary documents

Find the information you need to prepare a cash flow statement on the company's balance sheet and income statement. The balance sheet shows the company's assets and liabilities, while the income statement shows expenses and revenue.

Start with net income

Place the net income for the current financial period on the first line of the cash flow statement. You can list gains or losses on each line below this figure, adding or subtracting their totals from the net income as you go. Show deductions by placing them in parentheses.

List non-cash operating activities

Add or subtract from the net income noncash gains, losses or expenses, including depreciation, amortization, depletion, gains or losses from asset sales and losses from accounts receivable. Group all depreciation expenses (assets' reduced value over time) and use that total as your depreciation figure.

List cash operating activities

Then, list on each subsequent line all cash gains or losses, including expenses, inventory and accounts receivable. When adjusting the net income for cash gains and losses, subtract asset increases from the income and add asset decreases to the income.

List liabilities

For the last part of the operating activities section of the cash flow statement, you must adjust net income for cash changes to liability accounts such as accounts payable and accrued expenses. Liability adjustments are the opposite of asset adjustments. You add liability increases to the net income and subtract liability decreases from the income.

Calculate operating adjustments

Place the total of all the adjustments in this section on a line labeled "Net cash from operating activities."

Add investing activities

In the second section of the cash flow statement, simply add or subtract all investing activities, such as buying or selling stock or assets, for the period to calculate net cash from investing activities.

Add financing activities

In this section, add or subtract all actions the company has made to finance its operations for the period to calculate net cash from financing activities.

Calculate net increase or decrease

Add the totals from the operating, investing and financing sections together to get the company's net increase or decrease in cash.

Determine the cash balance

On the last lines of the statement, list the beginning (opening) cash balance, adjust it for the net increase or decrease amount and list that adjusted figure as the ending (closing) cash balance on the next line. The beginning and ending balance amounts are useful for assessing financial performance over time.

You can create a cash flow statement by hand, on a computer spreadsheet or using online tools and software programs that show you where to input information and perform the calculations for you.

Solution for #32

Practice quiz 1

For all questions assume that the indirect method is used.

There are four parts to the Statement of Cash Flows (or Cash Flow Statement):

1. Operating Activities

2. Investing Activities

3. Financing Activities

4. Supplemental Disclosures

For each of the following items, indicate which part will be affected.- 1.

Depreciation Expense.

OperatingInvestingFinancingSupplemental - 2.

Proceeds from the sale of equipment used in the business.

OperatingInvestingFinancingSupplemental - 3.

The Loss on the Sale of Equipment in Question #2.

OperatingInvestingFinancingSupplemental - 4.

Declaration and payment of dividends on company's stock.

OperatingInvestingFinancingSupplemental - 5.

Gain on the Sale of Automobile formerly used in the business.

OperatingInvestingFinancingSupplemental - 6.

The proceeds from the sale of the automobile in Item #5.

OperatingInvestingFinancingSupplemental - 7.

An increase in the balance in a retailer's Merchandise Inventory.

OperatingInvestingFinancingSupplemental - 8.

An increase in the balance in Accounts Payable.

OperatingInvestingFinancingSupplemental - 9.

Retirement of long-term Bonds Payable.

OperatingInvestingFinancingSupplemental - 10.

Purchase of Treasury Stock (company's own stock).

OperatingInvestingFinancingSupplemental - 11.

The purchase of a new delivery truck to be used in the business.

OperatingInvestingFinancingSupplemental - 12.

A decrease in the balance of Accounts Receivable.

OperatingInvestingFinancingSupplemental - 13.

An increase in Bonds Payable (a long-term liability).

OperatingInvestingFinancingSupplemental - 14.

A decrease in the current asset account Prepaid Insurance.

OperatingInvestingFinancingSupplemental - 15.

A decrease in the current liability Income Taxes Payable.

OperatingInvestingFinancingSupplemental - 16.

The proceeds from issuing additional Common Stock.

OperatingInvestingFinancingSupplemental - 17.

The amortization of the cost of an intangible asset.

OperatingInvestingFinancingSupplemental - 18.

The exchange/conversion of long-term bonds into common stock.

OperatingInvestingFinancingSupplemental For items 19 - 30 indicate whether they will have a positive or negative EFFECT ON CASH.

A positive effect could also be thought of as a source of cash, an increase in cash, or a positive amount on the cash flow statement.

A negative effect could also be thought of as a use of cash, a decrease in cash, or a negative amount on the cash flow statement.

- 19.

An increase in the balance of Prepaid Insurance.

PositiveNegative - 20.

A decrease in Supplies on hand.

PositiveNegative - 21.

The proceeds from the sale of equipment formerly used in the business.

PositiveNegative - 22.

The Loss on the Sale of Equipment in the previous question.

PositiveNegative - 23.

An increase in the current liability Income Taxes Payable.

PositiveNegative - 24.

A decrease in Accounts Payable.

PositiveNegative - 25.

An increase in Accounts Receivable.

PositiveNegative - 26.

An increase in the current liability Warranty Liability.

PositiveNegative - 27.

Dividends declared and paid.

PositiveNegative - 28.

Proceeds from the issuance of Preferred Stock.

PositiveNegative - 29.

The Gain on the Sale of Equipment formerly used in the business.

PositiveNegative - 30.

An increase in the long-term asset Investment in Another Company.

PositiveNegative - 31.

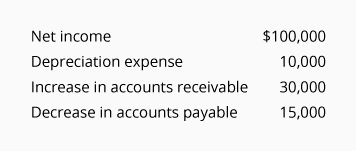

For a recent year a corporation's financial statements reported the following:

Based on the above information, what amount will the corporation report as Net Cash Provided by Operating Activities on the cash flow statement?$65,000$125,000$155,000 - 32.

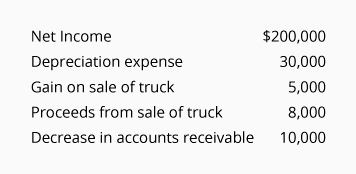

A corporation reported the following information for the past year:

Assuming these are the only facts, what amount will the corporation report as the Net Cash Provided by Operating Activities on the cash flow statement?$225,000$235,000$253,000 - 33.

Using the information in Question #32, what amount will be reported under Cash From Investing Activities?

$3,000$8,000$13,000

| 1 | ||||

| Evaluate only the company's ability to have sufficient cash for short-run needs | ||||

| Assess only the company's ability to meet its obligations and pay dividends | ||||

| Assess only the cash aspects of the company's investment and financing transactions for the period | ||||

| All of the above | ||||

| 2 | ||||

| $150,000 | ||||

| $1,000,000 | ||||

| $1,150,000 | ||||

| None of the amount | ||||

| 3 |  Assume all sales were credit sales. Calculate the amount of cash received from customers. | |||

| $620,000 | ||||

| $580,000 | ||||

| $630,000 | ||||

| $395,000 | ||||

| 4 | ||||

| ($95,000) | ||||

| ($93,000) | ||||

| ($97,000) | ||||

| Cannot be determined from information provided. | ||||

| 5 | ||||

| As an investing activity of $51,000 | ||||

| As a financing activity of $46,000 | ||||

| As a financing activity of $48,500 | ||||

| As an investing activity of $46,000 | ||||

| 6 | ||||

| The Financial Accounting Standards Board (FASB) recommends the direct method of reporting cash flows from operating activities. | ||||

| The majority of companies use the indirect method of reporting cash flows from operating activities. | ||||

| When the direct method is used to report the cash flows from operating activities, it must be shown that the amount is consistent with the amount reported under the indirect method. | ||||

| All of the above are true. | ||||

| 7 | ||||

| The indirect method adjusts accrual-basis net income to net cash flows from operating activities, but the direct method does not. | ||||

| The indirect method reports gain and losses on assets as cash flows from operating activities, but the direct method does not. | ||||

| The indirect method reports financing activities differently than the direct method. | ||||

| The indirect method ignores depreciation expense, but the direct method does not. | ||||

| 8 | ||||

| Deducted from the reported net income. | ||||

| Added to reported net income. | ||||

| Ignored. | ||||

| Shown as investing activities. | ||||

| 9 | ||||

| Deferring income taxes | ||||

| Changing credit policies from n60 to n30 | ||||

| Peak pricing | ||||

| Both (A) and (C) | ||||

| 10 |  Calculate the net cash flow from operating activities. | |||

| $350,000 | ||||

| $550,000 | ||||

| $230,000 | ||||

| $410,000 | ||||

1. Operating

ReplyDelete2. Investing

3. Operating

4. Financing

5. Operating

6. Investing

7. Operating

8. Operating

9. Financing

10. Financing

11. Investing

12. Operating

13. Financing

14. Operating

15. Operating

16. Financing

17. Operating

18. Supplemental

19. Negative

20. Positive

21. Positive

22. Positive

23. Positive

24. Negative

25. Negative

26. Negative

27. Negative

28. Positive

29. Negative

30. Negative

31. $65,000

32. $235,000

33. $8,000

BY : YENI PEREZ

26 is positive

Delete1. Operating

ReplyDelete2. Investing

3. Operating

4. Financing

5. Operating

6. Investing

7. Operating

8. Operating

9. Financing

10. Financing

11. Investing

12. Operating

13. Financing

14. Operating

15. Operating

16. Financing

17. Operating

18. Supplemental

19. Negative

20. Positive

21. Positive

22. Positive

23. Positive

24. Negative

25. Negative

26. Positive

27. Negative

28. Positive

29. Negative

30. Negative

31. $ 65,000… Sixty-five thousand

32. $235,000 Two hundred thirty five thousand

33. $8,000… Eigth thousand

(BY: Gisela Vargas)

1.Operating

ReplyDelete2.Investing

3.Operating

4.Financing

5.Operating

6.Investing

7.Operating

8.Operating

9.Financing

10.Financing

11.Investing

12.Operating

13.Financing

14.Operating

15.Operating

16.Financing

17.Operating

18.Supplemental

19.Negative

20.Positive

21.Positive

22.Positive

23.Positive

24.Negative

25.Negative

26.Positive

27.Negative

28.Positive

29.Negative

30.Negative

31.$65,000

32.$235,000

33.$8,000

BY: FARID PINEDO

For each of the following items, indicate which part will be affected.

ReplyDelete1. Operating

2. Investing

3. Operating

4. Financing

5. Operating

6. Investing

7. Operating

8. Operating

9. Financing

10. Financing

11. Investing

12. Operating

13. Financing

14. Operating

15. Operating

16. Financing

17. Operating

18. Supplemental

19. Negative

20. Positive

21. Positive

22. Positive

23. Positive

24. Negative

25. Negative

26. Negative

27. Negative

28. Positive

29. Negative

30. Negative

31. $65,000

32. $235,000

33. $8,000

BY :Jose rafael

This comment has been removed by the author.

ReplyDelete1. Operating

ReplyDelete2. Investing

3. Operating

4. Financing

5. Operating

6. Investing

7. Operating

8. Operating

9. Financing

10. Financing

11. Investing

12. Operating

13. Financing

14. Operating

15. Operating

16. Financing

17. Operating

18. Supplemental

19. Negative

20. Positive

21. Positive

22. Positive

23. Positive

24. Negative

25. Negative

26. Positive

27. Negative

28. Positive

29. Negative

30. Negative

31. $ 65,000

32. $235,000

33. $8,000

By:Lily Carrasco

1.Operating

ReplyDelete2.Investing

3.Operating

4.Financing

5.Operating

6.Investing

7.Operating

8.Operating

9.Financing

10.Financing

11.Investing

12.Operating

13.Financing

14.Operating

15.Operating

16.Financing

17.Operating

18.Supplemental

19.Negative

20.Positive

21.Positive

22.Positive

23.Positive

24.Negative

25.Negative

26.Positive

27.Negative

28.Positive

29.Negative

30.Negative

31.$65,000

32.$235,000

33.$8,000

by jeff echevarria

1. Operating

ReplyDelete2. Investing

3. Operating

4. Financing

5. Operating

6. Investing

7. Operating

8. Operating

9. Financing

10. Financing

11. Investing

12. Operating

13. Financing

14. Operating

15. Operating

16. Financing

17. Operating

18. Supplemental

19. Negative

20. Positive

21. Positive

22. Positive

23. Positive

24. Negative

25. Negative

26. Negative

27. Negative

28. Positive

29. Negative

30. Negative

31. $65,000

32. $235,000

33. $8,000

1- Operating

ReplyDelete2- Investing

3- Operating

4- Financing

5- Operating

6- Investing

7- Operating

8- Operating

9- Financing

10- Financing

11- Investing

12- Operating

13- Financing

14- Operating

15- Operating

16- Financing

17- Operating

18- Supplemental

19- Negative

20- Positive

21- Positive

22- Positive

23- Positive

24- Negative

25- Negative

26- Negative

27- Negative

28- Positive

29- Negative

30- Negative

31- $65,000

32- $235,000

33- $8,000

1. Operating

ReplyDelete2. Investing

3. Operating

4. Financing

5. Operating

6. Investing

7. Operating

8. Operating

9. Financing

10. Financing

11. Investing

12. Operating

13. Financing

14. Operating

15. Operating

16. Financing

17. Operating

18. Supplemental

19. Negative

20. Positive

21. Positive

22. Positive

23. Positive

24. Negative

25. Negative

26. Positive

27. Negative

28. Positive

29. Negative

30. Negative

31. $65,000

32. $235,000

33. $8,000

1.Operating

ReplyDelete2.Investing

3.Operating

4.Financing

5.Operating

6.Investing

7.Operating

8.Operating

9.Financing

10.Financing

11.Investing

12.Operating

13.Financing

14.Operating

15.Operating

16.Financing

17.Operating

18.Supplemental

19.Negative

20.Positive

21.Positive

22.Positive

23.Positive

24.Negative

25.Negative

26.Positive

27.Negative

28.Positive

29.Negative

30.Negative

31.$65,000

32.$235,000

33.$8,000

By: cristian calle

1. Operating

ReplyDelete2. Investing

3. Operating

4. Financing

5. Operating

6. Investing

7. Operating

8. Operating

9. Financing

10. Financing

11. Investing

12. Operating

13. Financing

14. Operating

15. Operating

16. Financing

17. Operating

18. Supplemental

19. Negative

20. Positive

21. Positive

22. Positive

23. Positive

24. Negative

25. Negative

26. Positive

27. Negative

28. Positive

29. Negative

30. Negative

31. $ 65,000

32. $235,000

33. $8,000

By: Frank Tantarico

1. Operating

ReplyDelete2. Investing

3. Operating

4. Financing

5. Operating

6. Investing

7. Operating

8. Operating

9. Financing

10. Financing

11. Investing

12. Operating

13. Financing

14. Operating

15. Operating

16. Financing

17. Operating

18. Supplemental

19. Negative

20. Positive

21. Positive

22. Positive

23. Positive

24. Negative

25. Negative

26. Positive

27. Negative

28. Positive

29. Negative

30. Negative

31. $ 65,000->Sixty-Five Thousand

32. $ 235,000 ->Two Hundred Thirty-Five Thousand

33. $ 8,000 ->Eight Thousand

by. giovany castillo

1. Operating

ReplyDelete2. Investing

3. Operating

4. Financing

5. Operating

6. Investing

7. Operating

8. Operating

9. Financing

10. Financing

11. Investing

12. Operating

13. Financing

14. Operating

15. Operating

16. Financing

17. Operating

18. Supplemental

19. Negative

20. Positive

21. Positive

22. Positive

23. Positive

24. Negative

25. Negative

26. Positive

27. Negative

28. Positive

29. Negative

30. Negative

31. $65,000

32. $235,000

33. $8,000

by(juanita tocas)

1-Operating

ReplyDelete2-Investing

3-Operating

4-Financing

5-Operating

6-Investing

7-Operating

8.Operating

9-Financing

10-Financing

11-Investing

12-Operating

13-Financing

14-Operating

15-Operating

16-Financing

17-Operating

18-Supplemental

19-Negative

20-Positive

21-Positive

22-Positive

23-Positive

24-Negative

25-Negative

26-Positive

27-Negative

28-Positive

29-Negative

30-Negative

31-$65,000

32-$235,000

33-$8,000

1. Operating.

ReplyDelete2. Investing.

3. Operating.

4. Financing.

5. Operating.

6. Investing.

7. Operating.

8. Operating.

9. Financing.

10. Financing.

11. Investing.

12. Operating.

13. Financing.

14. Operating.

15. Operating.

16. Financing.

17. Operating.

18. Supplemental.

19. Negative.

20. Positive.

21. Positive.

22. Positive.

23. Positive.

24. Negative.

25. Negative.

26. Positive.

27. Negative.

28. Positive.

29. Negative.

30. Negative.

31. $65,000.

32. $235,000.

33. $8,000.

By. Noli Cubas

1) Operating

ReplyDelete2) Investing

3) Operating

4) Financing

5) Operating

6) Investing

7) Operating

8) Operating

9) Financing

10) Financing

11) Investing

12) Operating

13) Financing

14) Operating

15) Operating

16) Financing

17) Operating

18) Supplemental

19) Negative

20) Positive

21) Positive

22) Positive

23) Positive

24) Negative

25) Negative

26) Positive

27) Negative

28) Positive

29) Negative

30) Negative

31) $65,000

32) $235,000

33) $8,000

BY: MAGDIEL

This comment has been removed by the author.

ReplyDelete1_Operating.

ReplyDelete2_Investing.

3_Operating.

4_Financing.

5_Operating.

6_Investing.

7_Operating.

8_Operating.

9_Financing.

10_Financing.

11_Investing.

12_Operating.

13_Financing.

14_Operating.

15_Operating.

16_Financing.

17_Operating.

18_Supplemental.

19_Negative.

20_Positive.

21_Positive.

22_Positive.

23_Positive.

24_Negative.

25_Negative.

26_Negative.

27_Negative.

28_Positive.

29_Negative.

30_Negative.

31_$ 65,000

32_$ 235,000

33_$ 8,000

By : Ary GT

1.Operating

ReplyDelete2.Investing

3.Operating

4.Financing

5.Operating

6.Investing

7.Operating

8.Operating

9.Financing

10.Financing

11.Investing

12.Operating

13.Financing

14.Operating

15.Operating

16.Financing

17.Operating

18.Supplemental

19.Negative

20.Positive

21.Positive

22.Positive

23.Positive

24.Negative

25.Negative

26.Positive

27.Negative

28.Positive

29.Negative

30.Negative

31.$65,000

32.$235,000

33.$8,000

By : Keisy López Vásquez

1.Operating

ReplyDelete2.Investing

3.Operating

4. Financiación

5.Operating

6.Investing

7.Operating

8.Operating

9.Financing

10.Financing

11.Investing

12.Operating

13.Financing

14.Operating

15.Operating

16.Financing

17. Operativo

18.Suplemental

19.Negativo

20.Positivo

21.Positivo

22.Positivo

23.Positivo

24.Negativo

25.Negativo

26.Positivo

27.Negativo

28.Positivo

29.Negativo

30.Negativo

31. $ 65.000

32. $ 235.000

33. $ 8.000

by: Alonso Saboya

1.Operating

ReplyDelete2.Investing

3.Operating

4. Financiación

5.Operating

6.Investing

7.Operating

8.Operating

9.Financing

10.Financing

11.Investing

12.Operating

13.Financing

14.Operating

15.Operating

16.Financing

17. Operativo

18. Suplementario

19.Negativo

20.Positivo

21.Positivo

22.Positivo

23.Positivo

24.Negativo

25.Negativo

26.Positivo

27.Negativo

28.Positivo

29.Negativo

30.Negativo

31. $ 65.000

32. $ 235.000

33. $ 8.000

(Fiorela Mendez)

1) Operating

ReplyDelete2) Investing

3) Operating

4) Financing

5) Operating

6) Investing

7) Operating

8) Operating

9) Financing

10) Financing

11) Investing

12) Operating

13) Financing

14) Operating

15) Operating

16) Financing

17) Operating

18) Supplemental

19) Negative

20) Positive

21) Positive

22) Positive

23) Positive

24) Negative

25) Negative

26) Positive

27) Negative

28) Positive

29) Negative

30) Negative

31) $ 65,000

32) $235,000

33) $8.000

By: Paola Aguilar

1_Operating.

ReplyDelete2_Investing.

3_Operating.

4_Financing.

5_Operating.

6_Investing.

7_Operating.

8_Operating.

9_Financing.

10_Financing.

11_Investing.

12_Operating.

13_Financing.

14_Operating.

15_Operating.

16_Financing.

17_Operating.

18_Supplemental.

19_Negative.

20_Positive.

21_Positive.

22_Positive.

23_Positive.

24_Negative.

25_Negative.

26_Negative.

27_Negative.

28_Positive.

29_Negative.

30_Negative.

31_$ 65,000

32_$ 235,000

33_$ 8,000

1) Operating

ReplyDelete2) Investing

3) Operating

4) Financing

5) Operating

6) Investing

7) Operating

8) Operating

9) Financing

10) Financing

11) Investing

12) Operating

13) Financing

14) Operating

15) Operating

16) Financing

17) Operating

18) Supplemental

19) Negative

20) Positive

21) Positive

22) Positive

23) Positive

24) Negative

25) Negative

26) Positive

27) Negative

28) Positive

29) Negative

30) Negative

31) $ 65,000

32) $235,000

33) $8,000

By Rocio Sanchez

1) Operating

ReplyDelete2) Investing

3) Operating

4) Financing

5) Operating

6) Investing

7) Operating

8) Operating

9) Financing

10) Financing

11) Investing

12) Operating

13) Financing

14) Operating

15) Operating

16) Financing

17) Operating

18) Supplemental

19) Negative

20) Positive

21) Positive

22) Positive

23) Positive

24) Negative

25) Negative

26) Positive

27) Negative

28) Positive

29) Negative

30) Negative

31) $ 65,000

32) $235,000

33) $8,000

BY: RUTH CRISTINA

Quiz 2

ReplyDelete1.B

2.A

3.A

4.B

5.B

6.D

7.A

8.A

9.D

10.A

BY: FARID PINEDO

1. B

ReplyDelete2. A

3. A

4. B

5. B

6. D

7. A

8. A

9. D

10. A

BY: Gisela Vargas

1. B

ReplyDelete2. A

3. A

4. B

5. B

6. D

7. A

8. A

9. D

10. A

B

ReplyDeleteA

A

B

B

D

A

A

D

A

(Fiorela Mendez)

quiz 2

ReplyDelete1_B

2_A

3_A

4_B

5_B

6_D

7_A

8_A

9_D

10_A

by ary

by: FELIX RAMIREZ

ReplyDelete1. B

2. A

3. A

4. B

5. B

6. D

7. A

8. A

9. D

10. A

1) B

ReplyDelete2) A

3) A

4) B

5) B

6) D

7) A

8) A

9) D

10) A

By: Paola Aguilar

1.B

ReplyDelete2.A

3.A

4.B

5.B

6.D

7.A

8.A

9.D

10.A

By: Damaris Ivonn Alvites Vasquez

1) B

ReplyDelete2) A

3) A

4) B

5) B

6) D

7) A

8) A

9) D

10) A

1=B

ReplyDelete2=A

3=A

4=B

5=B

6=D

7=A

8=A

9=D

10=A

BY: RUTH CRISTINA

1) operating

ReplyDelete2) Investing

3) operating

4) Financing

5) operating

6) Investing

7) operating

8) operating

9) Financing

10) Financing

11) Investing

12) operating

13) Financing

14) operating

15) operating

16) Financing

17) operating

18) Supplemental

19) Negative

20) Positive

21) Positive

22) Negative

23) Positive

24) Negative

25) Negative

26) Positive

27) Negative

28) Positive

29) Negative

30) Negative

31) $ 65,000

32) $ 235,000

33) $8,000

BY: merli cotrina

1) B

ReplyDelete2) A

3) A

4) B

5) B

6) D

7) A

8) A

9) D

10) A

By Rocio Sanchez

By : Yeni Perez

ReplyDelete1.b

2.a

3.a

4.b

5,b

6.d

7.a

8.a

9.d

10.a

Quiz 2

ReplyDelete1.(b)

2.(a)

3.(a)

4.(b)

5.(b)

6.(d)

7.(a)

8.(a)

9.(d)

10.(a)

by jeff echevarria

1.B

ReplyDelete2.A

3.A

4.B

5.B

6.D

7.A

8.A

9.D

10.A

by: cristian calle

by giovany castillo

ReplyDelete1. B

2. A

3. A

4. B

5. B

6. D

7. A

8. A

9. D

10.A

B

ReplyDeleteA

A

B

B

D

A

A

D

A

BY(Juanita Tocas)

1) B

ReplyDelete2) A

3) A

4) B

5) B

6) D

7) A

8) A

9) D

10) A

BY MAGDIEL

1. B

ReplyDelete2. A

3. A

4. B

5. B

6. D

7. A

8. A

9. D

10. A

BY: merli cotrina

1.B

ReplyDelete2.A

3.A

4.B

5.B

6.D

7.A

8.A

9.D

10.A

By: Frank Tantarico

-1.B

ReplyDelete-2.A

-3.A

-4.B

-5.B

-6.D

-7.A

-8.A

-9.D

-10.A

By: Jose rafael"

1. B.

ReplyDelete2. A.

3. A.

4. B.

5. B.

6. D.

7. A.

8. A.

9. D.

10. A.

By. Noli Cubas

1. B.

ReplyDelete2. A.

3. A.

4. B.

5. B.

6. D.

7. A.

8. A.

9. D.

10. A.

By: JESÚS HUAMAN

1Operating

ReplyDelete2 Investing

3 Operating

4 Financiación

5 Operating

6 Investing

7 Operating

8 Operating

9 Financing

10 Financing

11 Investing

12 Operating

13 Financing

14 Operating

15 Operating

16 Financing

17 Operativo

18 Suplementario

19 Negativo

20 Positivo

21 Positivo

22 Positivo

23 Positivo

24Negativo

25 Negativo

26 Positivo

27 Negativo

28 Positivo

29negativo

30 Negativo

31 $ 65.000

32 $ 235.000

33 $ 8.000

1-B

ReplyDelete2-A

3-A

4-B

5-B

6-D

7-A

8-A

9-D

10-A

By Widman

This comment has been removed by the author.

ReplyDelete1.Operating

ReplyDelete2.Investing

3.Operating

4. Financiación

5.Operating

6.Investing

7.Operating

8.Operating

9.Financing

10.Financing

11.Investing

12.Operating

13.Financing

14.Operating

15.Operating

16.Financing

17. Operativo

18.Suplemental

19.Negativo

20.Positivo

21.Positivo

22.Positivo

23.Positivo

24.Negativo

25.Negativo

26.Positivo

27.Negativo

28.Positivo

29.Negativo

30.Negativo

31. $ 65.000

32. $ 235.000

33. $ 8.000

1._B

ReplyDelete2._A

3._A

4._B

5._B

6._D

7._A

8._A

9._D

10._A

by: Deanelli Julca

1: B

ReplyDelete2: A

3: A

4: B

5: B

6: D

7: A

8: A

9: D

10: A

by: Linda Gutarra

Quiz 2

ReplyDelete1.B

2.A

3.A

4.B

5.B

6.D

7.A

8.A

9.D

10.A

1: Operating

ReplyDelete2: Investing

3: Operating

4: Financiación

5: Operating

6: Investing

7: Operating

8: Operating

9: Financing

10: Financing

11: Investing

12: Operating

13: Financing

14:Operating

15:Operating

16:Financing

17: Operativo

18:Suplemental

19:Negativo

20:Positivo

21:Positivo

22:Positivo

23:Positivo

24:Negativo

25:Negativo

26:Positivo

27:Negativo

28:Positivo

29:Negativo

30:Negativo

31: $ 65.000

32: $ 235.000

33: $ 8.000

by: Linda Gutarra

QUIZ 2:

ReplyDelete1. B

2. A

3. A

4. B

5. B

6. D

7. A

8. A

9. D

10. A

1. B

ReplyDelete2. A

3. A

4. B

5. B

6. D

7. A

8. A

9. D

10. A

By :Lily Carrasco

1-B

ReplyDelete2-C

3-C

4-D

5-C

6-D

7-D

8-B

9-D

10-D

By Keisy López

ReplyDelete1. B

2. A

3. A

4. A

5. B

6. D

7. A

8. A

9. D

10. A

By: Alessandro Gomez

ReplyDelete1. Operating

2. Investing

3. Operating

4. Financing

5. Operating

6. Investing

7. Operating

8. Operating

9. Financing

10. Financing

11. Investing

12. Operating

13. Financing

14. Operating

15. Operating

16. Financing

17. Operating

18. Supplemental

19. Negative

20. Positive

21. Positive

22. Positive

23. Positive

24. Negative

25. Negative

26. Positive

27. Negative

28. Positive

29. Negative

30. Negative

31. $65,000

32. $235,000

33. $8,000